There was a lot going on in mid-March and I somehow forgot to add a post when the government announced that it was ending its student loan sale programme.

I had predicted this in January and that post contains a full explanation as to why such a decision was likely.

In short, it’s because there was no longer a presentational advantage from the sale and the accounting change introduced by the ONS meant that the losses on sales (the difference between cash raised and book value) now hit the headline fiscal statistics.

The Committee of University Chairs has published an updated Governance Code.

I’ve worked extensively with union branches over the last year and I think one points is worth citing from the Code, since it warns against behaviour seen at some universities.

There is only one category of governor / trustee, regardless of how they are appointed to the governing body.

§1.4 All members of the governing body (including students and staff members) share the same legal responsibilities and obligations as other members, so no one can be routinely excluded from discussions. All members have a duty to record and declare any conflicts of interest.

I would add to my emphasis above by suggesting that this also means that members who are elected by staff or nominated by trade unions should not be prevented from seeing papers that have gone to committees.

§3.2 Members of governing bodies need to act, and be perceived to act, impartially, and not be influenced by social or business relationships. Institutions must maintain, check and publish a register of the interests of members and senior executives.

A member who has a professional, pecuniary, family or other personal interest in any matter under discussion which may be seen to conflict with the best interests of the institution must also disclose the interest in advance of any discussion on the topic.

A member does not have a pecuniary interest merely because they are a member of staff or a student.

(Again my emphasis.)

After my July UCU presentation on institutional finances, I was asked what the situation in Wales was with regard to liquidity and regulation.

Office for Students currently requires institutions to alert them if liquidity falls below 30 days.* This “reportable event” is designed to give the regulator notice that intervention might be required or a “market exit” managed.

It is not to be confused with a prudent level of liquidity. Most universities would specify the equivalent of 45-60 days as required for the “working capital” needed to cover daily activities.

The HEFCW Financial Management Code doesn’t specify a minimum level, but requires Welsh HEIs to be more liquid.

86f. The institution must ensure that it retains sufficient liquid cash or equivalents to service working capital requirements as well as a prudent level of liquid reserve to be called upon in the case of extraordinary events;

This reference to prudence indicates that Welsh regulation is still aligned with Charity Commission guidance for charities to be able to cover 90 days of expenditure. Or more pointedly, it indicates the difference between the regulation of a quasi-public service and the market competition seen in England.

Some English universities did reason that they didn’t need to have so much cash and near-cash to hand as they weren’t reliant on donations and so income was more predictable.

The last few months have undermined that argument: projected income for 2020/21 has moved dramatically. Those institutions without significant liquidity (which can incorporate overdrafts and revolving credit facilities) were moved to push the expected shock from Covid on to operating budgets and staff pay and conditions. This was clearly bad practice and has affected staff goodwill, even if budgets now look very different for this financial year.

If universities manage to avoid a financial shock from the pandemic, many need to recognise that they were not in a good position. The idea that liquid reserves hoard resources that would be better invested in buildings seems to have had widespread currency. This year should really produce a rethink about the merits of “efficient” or “lean” approaches to treasury practice.

Had the pandemic arrived with the kind of impact that many universities were modelling, then some would have been lucky or unlucky depending on where they were in their capital development cycle. If they had borrowed to invest and not yet spent the money, they would have got through. If they had spent the money …

That’s not good enough. It’s bad governance not to have contingency or “rainy days” funds.

*The “liquidity days” measure calculates the number of days of average expenditure that an institution can cover from cash and current investments (things that can be readily turned into cash like deposit accounts with notice periods) if income were to dry up. It measures the ability to deal with a short-term shock.

Calculations vary but a typical measure would see annual operating expenditure less depreciation and adverse pension movements (both non-cash expenditure items) divided by 365 to give the average daily expenditure. The amount of cash and current investments on hand can be then be used to arrive at the number of days that can be covered.

Private Eye (3-16 July) picked up on a report I wrote for Sussex UCU back in May.

These reports are normally confidential and used to inform negotiations.

If your branch is looking for some analysis, please let me know. I might have some time in August.

I ran a webinar for UCU on Wednesday 8 July covering some basics on university finances.

It was recorded and can be found here along with the slides I used. We were originally planning to run training days in April and May, so this 90min presentation with questions is a little quick.

It followed on from a blog I did for UCU on the same topic.

Here is a link to a guest post I have written for UCU’s “Fund the Future” campaign.

https://fundthefuture.org.uk/challenging-the-financial-narrative/

I will be participating in a webinar next Wednesday lunchtime for UCU branch officials on university finances. You can get details from your Regional officers.

… the greatest problem of the guerrilla band is the lack of ammunition, which the opponent must provide.

UCU branches that are recognised will have an agreement with clauses pertaining to the disclosure of information for bargaining and consultation.

We are currently in a situation where it is not possible to rely on published sources of financial information. Universities publish accounts once per year. The latest such accounts should have appeared in December and cover the year to 31 July 2019. That is, they are over nine months out of date and were in any case retrospective. Moreover, they are “pre-covid”.

As universities consider the potential hits to income for the next academic year and try to draw up budgets, they will have prepared financial scenarios. UCU branches should be requesting these. It’s not possible to assess any proposals put forward by management without the ability to interrogate the assumptions and models. It’s also important to check that you are seeing the same range of scenarios as governors and regulators.

Where an employer refuses to disclose essential information, the recognised trade union has the right to complain to the Central Arbitration Committee, who have the power to adjudicate and require compliance with their judgments.

I won a case at the CAC about 20 years ago. My chief memory of it was the delay in having the case heard, so it is better to get a complaint in early. But it was possible to get the employer to produce data and information , even where it wasn’t necessarily to hand (as in my case: a breakdown of starting salaries by sex and ethnicity in different departments). It was also relatively easy process and hearing for an amateur like me to navigate.

CAC’s Code of Practice on information disclosure is extremely useful and gives examples of the kind of information it considers pertinent to bargaining (section 11).

iv) Performance: productivity and efficiency data; savings from increased productivity and output, return on capital invested; sales and state of order book.

(v) Financial: cost structures; gross and net profits; sources of earnings; assets; liabilities; allocation of profits; details of government financial assistance; transfer prices; loans to parent or subsidiary companies and interest charged.

I would take “state of the order book” to be analogous to what universities are currently fretting over.

Note that the restrictions on the “general duty” to disclose (sections 13ff.) set a much higher bar for the employer than the equivalent exemptions for Freedom of Information, which has a different emphasis on publication and public interest. The assumption would be that the information disclosed for bargaining purposes may have conditions set on how and how far it can be disseminated. I would say you should be looking to invoke these disclosure of information rights over FoI.

Given that you need to put your request for information in writing to management (and give them suitable period by which to respond), I would recommend considering the option early.

It’s very apparent across the sector that different institutions take very different approaches to the disclosure of information, but it is essential to know what recourse you might have.

If anyone has more recent experience of complaining to the CAC, please let me know, either privately or in the comments below.

And obviously there are plenty of other documents you might need sight of. A look through papers going to Board/Council and the audit, risk and finance committees will help here.

update 9 July 2020

In the section quoted above from the CAC Code of Practice, I would take “liabilities” to cover debt and debt covenants.

I was hoping to have been able to announce a couple of new initiatives, but world events have postponed them.

I can write about one of them. I had agreed to deliver some training events for UCU, designed to explain accounting to officers and branch activists and explain methods of getting information out of university management. The first three events should have started this month.

If you have general questions about university accounts and financial information, then you can post them here or email me and I will try to answer some questions through the blog. If I have time, I will try to make some of my training materials available on this site.

I am still taking commissions for in-depth and “scoping” reports on individual universities. If you think you might want some help working out how coronavirus is going to affect your institutional finances, do drop me a line. In general, I think the sector has been far too casual about the vulnerabilities in the standard business model and many universities were already struggling before the virus arrived. I was already expecting our first “market failures” / interventions of the new funding regime this calendar year.

Happy New Year!

This blog has now been running for nearly nine years. In recent months, the output has slowed and I see that I haven’t done anything since September.

In the main, this is because work elsewhere is keeping from writing. I think that is likely to continue in the near future: I will mainly be producing private commissioned reports for UCU branches following the publication of the latest round of annual reports.

I will probably fire up this blog again in March for the budget and later that month, when I should be able to say more about a couple of new initiatives.

In the meantime, here is the latest odd development in the ongoing saga of Reading’s National Institute for Research in Dairying Trust. The headline captures it: “Dead Radioactive Goats Experimented on Decades Ago Could be Buried in Berkshire”. More precisely, in Shinfield.

Proceeds from that sale of Shinfield land was subsequently passed on by the trust to the university. Reading’s latest accounts tell us that the matter of this multimillion pound loan from the trust to the university is still not resolved:

“”During the year, the University and one of its connected trusts, the National Institute for Research in Dairying Trust (NIRD), have been in discussions to resolve some legacy governance issues that were self-reported to OfS and the Charity Commission. These discussions are progressing well and are still ongoing. To date, they have not raised any issues that would have a material impact on the University. The University is the sole Trustee of NIRD, and NIRD is accounted for as part of the University group.”

At the national level, the announced change to the government’s fiscal rules makes it more likely that the programme of student loan sales will come to an end. The ONS announced that the two sales so far completed have lost £2.7billion and that this will now count as capital expenditure in the national accounts.

Now that the government has decided to stop targeting Public Sector Net Debt as part of its fiscal mandate, the main aim of the loan sale loses much of its point. As explained here (and elsewhere) over the years, the fiscal illusion embedded in the composition of PSND (not changed by the ONS’s recent accounting overhaul) means that student loans are not counted as an asset in that headline figure. Any sale thereby improves PSND as the cash raised does count: PSND is reduced whatever loss is registered on the loans. What has changed is that the loss now scores as expenditure.

PSND is now sidelined and the losses on sales count as expenditure against the new secondary target of Public Sector Net Investment (3% of GDP per year). That would seem to mean that the sale programme performs badly against what are effectively the government’s chosen performance targets.

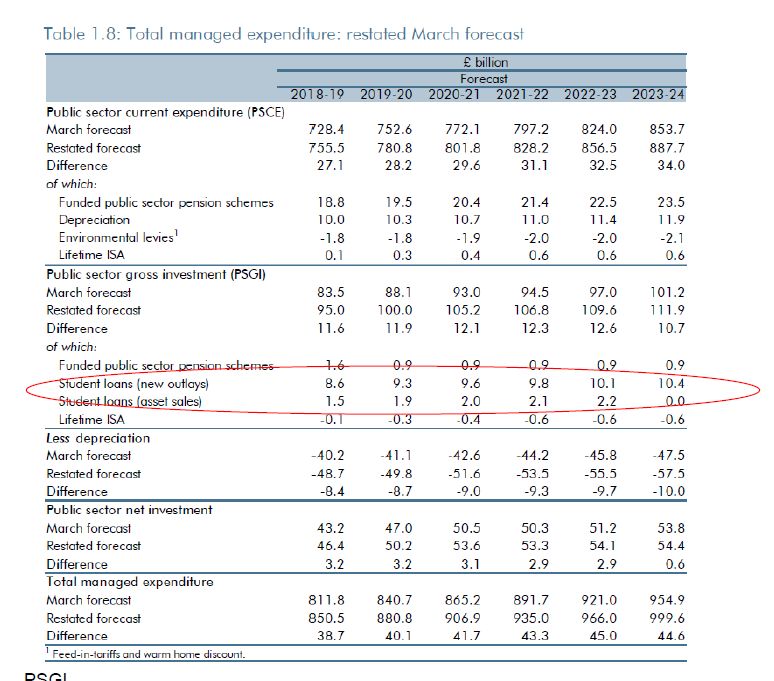

That PSNI target already has to accommodate the c. £10bn pa needed to fund estimated write-offs on new loans. For more detail on those impacts, seethe Office for Budget Responsibility’s restated March 2019 forecasts(from which the table below is taken).

Unlike in 2017 and 2018, there was no sale in December. The Budget would be the normal occasion on which the Chancellor would confirm whether or not they are still going ahead.

Now that the accounting more accurately reflects the impact of the decision to sell or not, you would expect reason to prevail and the scheme to be halted.

Everyone’s attention was elsewhere yesterday, but ONS’s monthly release on public finances included its promised update on the inclusion of student loans in the national accounts.

Its new methodology had been confirmed in July, but the relevant statistics were only updated in the new release. In addition to retrospective revisions of Public Sector Net Borrowing (back to 1999/2000), ONS announced that on their new approach the two sales of income contingent repayment loans had “lost” £1.2billion and £1.5billion respectively and that these sums had also been added to the deficit for 2017/18 and 2018/19 respectively.

I use “lost”, but the ONS put it as follows:

Where we identify that the sale price was significantly different from the value recorded in the national accounts balance sheet, we record a capital transfer equal to the difference in value between the realised sale proceeds and our estimate of the corresponding loan asset’s value, which affects PSNB.

Our analysis of the pre-2012 loan sales that took place in December 2017 and December 2018 shows that the difference in value on those occasions was £1.2 billion in 2017 and £1.5 billion in 2018; we recorded capital transfers of those amounts for each of the loan sales. (my emphasis)

The point being that the loans were sold for less than ONS thought they were worth.

National accounts are UK-wide and work differently to departmental accounts. These points explain the discrepancy between the £2.7billion sum above and the £2billion loss recorded in the Department for Education’s accounts. DfE only has responsibility for “English” loans (loans made to English-domiciled students at UK universities and EU students at English universities). Either way, it’s a significant loss: over 50 Garden Bridges.

As a result of the classification changes to sales and general student loan accounting, the deficit for 2018/19 (year ending March 2019) was pushed up by £12.4billion. (The estimated loss on issuing loans is now counted as expenditure in the year that loans are issued, rather than in the year that they are written off and, as a corollary, the government is only allowed to count interest it expects to be paid as income – rather than all interest accruing).

The Office for Budgetary Responsibility has not yet incorporated the loan sale change into its projections for 2019/20 (presuming a third sale goes ahead), but it anticipates that the impact will be slightly higher. Student loans will anyway push up the projected deficit from under £30billion to over £40billion. Public Debt is unaffected by this change (there is still a fiscal illusion at work there insofar as student loans as an asset are excluded from the calculation).

Government had previously stated that a loan sale should have no negative impact on the deficit. And this was originally formalised as a criteria that any sale would have to meet. Now that sales do count, it is clearer that the programme is generating a loss. Sajid Javid may still push ahead after deciding that reducing the debt is more important. It is clear that the spending restrictions outlined in the Fiscal Mandate championed by the former chancellors, Hammond and Osborne, are falling by the wayside. See my recent piece for London Review of Books for more detail.

In general, we now have national accounts that better reflect the nature of student loans at the time the loans are issued and capture the impact of sales. The opportunism of previous administrations is now curtailed and we can be a little more assured that the presentational advantages of certain policies have diminished.

To speak from a personal perspective, we now have an approach to sales for which I argued back in 2017. Sales are now being treated as “capital transfers”, rather than “revaluations”. And we have now resolved most of the issues I raised at the Treasury and Economic Affairs committees back then.

More concretely, these changes mean that alternative proposals such as Labour’s pledge to abolish tuition fees become easier to implement, given the manner in which questions of fiscal competence have become focused on the “deficit” as measured by PSNB. In particular, a costing similar to the one prepared for Labour’s 2017 manifesto now becomes easier, because things that weren’t counted as expenditure previously now are and so can be offset against replacement policies. I will talk about this in a subsequent blog in relation to the Institute for Fiscal Study’s annual education report, which was published last week.