Calculator Caveats

Update – 2 May 2016. Josh Winn has pointed out to me that the SLC is currently offline. Hopefully this is because SLC has taken the points below onboard. I have asked SLC for comment.

Update – 11 May 2016. SLC have replied to my query with the following statement: “The Repayment Calculator has been removed temporarily from the Student Loans Repayments website and gov.uk for maintenance and enhancement.”

Income contingent repayment loans are fundamentally different from any other loan or debt you are likely to encounter.

Student loans have additionally been designed to protect lower earners from unaffordable repayments and so have a high repayment threshold – you repay 9 per cent of your gross annual income above £21 000.

So if you earn £30 000 in a year you repay 9% of £9000 – £810. If you earn £21 000 no repayment is due.

In addition, outstanding loan balances are written off in the event of death, disability or thirty years after repayments first fall due (the April after you leave study).

Because repayments are contingent upon income, predicting how much you are likely to repay (the price of study) is difficult. You have to make a lot of assumptions about your future salary path and various economic variables (inflation, average earnings, etc.)

What guidance can you get in this regard? There are two kinds of ‘calculator’ in existence.

One is used to model the cost to government of the student loan policy. Here cost is the difference between what is loaned and what is repaid in net present value terms.

The other kind is aimed at individuals and asks them to input a starting salary and initial student debt before calculating an estimate of repayments in cash terms.

This website has mainly been concerned with the first kind of calculator but I have recently started looking at the second kind.

Today, I want to warn people about using the calculator provided by the Student Loans Company.

This is the worst one I have seen – mainly because it provides such limited information about its questionable assumptions.

These calculators are designed to inform you about your likely repayments, but the SLC calculator probably overestimates these for two reasons:

- it assumes you are male;

- it assumes large increments in salary in the first years after graduation regardless of the starting salary you input

Although I asked SLC for its modelling assumptions, I did not get answers to my specific questions. I was though able to access the code for the calculator.

The code is helpfully annotated so that it is clear that its assumptions about average graduate salary increments are labelled ‘Medium male data’. Each figure in the array reproduced below is an annual increase to be calculated in addition to average earnings growth. Some of the years are negative, indicating that graduate salaries increase by less than average earnings.

Average earnings growth is assumed to be 4.4 per cent throughout. Though the most recent OBR Economic and Fiscal Outlook reports:

1.15 On an annual basis, headline average weekly earnings growth slowed from a recent peak of 3.0 per cent in September to just 1.9 per cent in the latest data.

And estimates that earnings growth will return to around 3.5 per cent for the medium term.

SLC array for graduate salary increments – negative values highlighted in bold

// Medium male data

var SalaryAvgGrowthRate = new Array();

SalaryAvgGrowthRate[0] = 0;

SalaryAvgGrowthRate[1] = 16.456;

SalaryAvgGrowthRate[2] = 13.587;

SalaryAvgGrowthRate[3] = 9.569;

SalaryAvgGrowthRate[4] = 6.987;

SalaryAvgGrowthRate[5] = 7.347;

SalaryAvgGrowthRate[6] = 5.323;

SalaryAvgGrowthRate[7] = 3.971;

SalaryAvgGrowthRate[8] = 4.861;

SalaryAvgGrowthRate[9] = 1.987;

SalaryAvgGrowthRate[10] = 2.273;

SalaryAvgGrowthRate[11] = 0.952;

SalaryAvgGrowthRate[12] = 1.258;

SalaryAvgGrowthRate[13] = 0.932;

SalaryAvgGrowthRate[14] = -0.308;

SalaryAvgGrowthRate[15] = 0.617;

SalaryAvgGrowthRate[16] = 1.534;

SalaryAvgGrowthRate[17] = 0.302;

SalaryAvgGrowthRate[18] = -2.108;

SalaryAvgGrowthRate[19] = 0.308;

SalaryAvgGrowthRate[20] = 0.613;

SalaryAvgGrowthRate[21] = 1.22;

SalaryAvgGrowthRate[22] = 0;

SalaryAvgGrowthRate[23] = 0.602;

SalaryAvgGrowthRate[24] = 1.796;

SalaryAvgGrowthRate[25] = -2.059;

SalaryAvgGrowthRate[26] = 0.901;

SalaryAvgGrowthRate[27] = 2.381;

SalaryAvgGrowthRate[28] = 0;

SalaryAvgGrowthRate[29] = 0.291;

SalaryAvgGrowthRate[30] = -1.739;

SalaryAvgGrowthRate[31] = -0.59;

SalaryAvgGrowthRate[32] = 0.297;

SalaryAvgGrowthRate[33] = -2.071;

SalaryAvgGrowthRate[34] = -2.417;

http://www.studentloanrepayment.co.uk/scheme/rep/repayment-calculator/sfe/js/repaymentCalculator.js

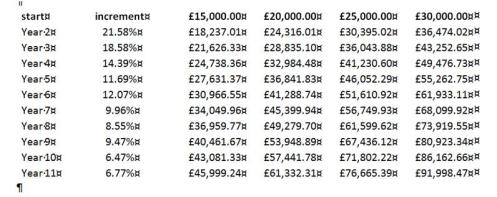

Applying the increment schedule to the average earnings growth provides us with an indicative schedule of increments ([1+Grad increment /100 ]* 1.044). In the table below I’ve applied the annual increment calculated for the first decade after finishing studies for four different starting salaries.

This looks unrealistic to me. And with such optimistic outlooks for salaries, repayments will be likely be overstated.

The Student Loans Company provided me with the following statements:

What are the assumptions on graduate salary pathways in the calculator? The calculator asks for a starting salary but does not specify how it then calculates future annual earnings. The increments appear to be quite steep (c£5000 pa).

All assumptions regarding earnings are provided by the Office of National Statistics (ONS); the data is forecasted and is to be used only as a guide.

Is the calculator designed to show a high-end estimate of repayments?

The calculator is intended to be used by prospective borrowers to give them an indication of potential repayments only, it cannot be used as a personal quotation tool, as it does not take into account the reality of variable salaries and individual circumstances after graduation.

When all is said and done, the SLC as the administrator of loans needs to establish best practice in this area of information provision. It needs to do so by making its own assumptions and caveats explicit on the website – not just in statements to the press.

It becomes a more pressing issue as alternative financial products pitched at potential students come on to the market. They will use these SLC figures as the official ‘cost’ of study and present their products accordingly.

Having an SLC calculator that overstates costs may mislead students into choosing more expensive options. (As an aside, estimating cost rather than cash repayments involves adopting an appropriate discount rate to assess the value of each future repayment).

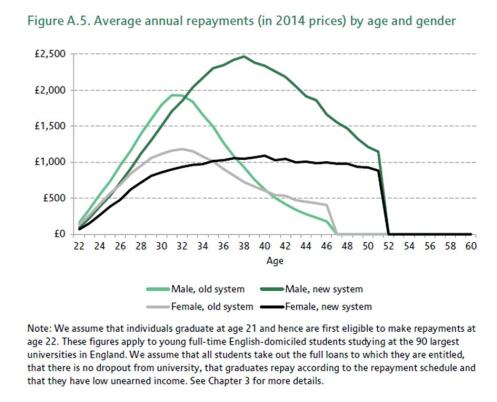

Average annual repayments by sex

Women in particular should be wary of alternative financial products that do not offer repayment threshold or balance write-offs.

The figure below is taken from a recent Institute for Fiscal Studies publication. It shows the differences in average annual repayments made by men and women on their modelling. This difference in average repayments reflects differences in employment patterns and earnings by sex.

Claire Crawford & Wenchao Jin Payback time? Student debt and loan repayments: what will the 2012 reforms mean for graduates? Institute of Fiscal Studies April 2014, p47

Acknowledgements

Thanks to Rich Cochrane and Gavan Conlon for assistance.

Reblogged this on Critical Education and commented:

reblogged because it looks like SLC have taken the calculator down.

Even if one knew one’s future income, and future RPI rates, there would be no certainty about how much the repayments would be. This is because Government has now set a precedent – they can and have changed the loans terms retrospectively