Sale of Student Loans

The 2015/16 BIS accounts state that a first sale of ‘pre-2012’ income contingent student loans is planned for 2016/17.

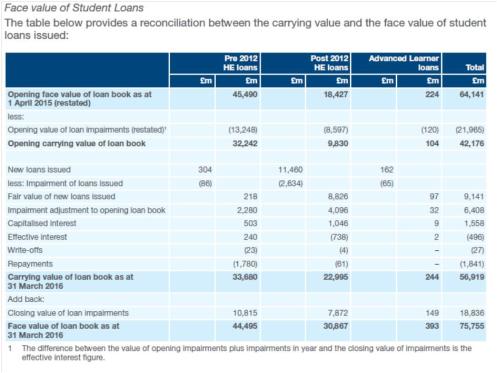

For the first time, the BIS accounts breakdown the loan book into ‘pre-2012’ and ‘post-2012’ loans, providing separate fair and face values for each category.

Click on image to enlarge

The fair value of loans earmarked for potential sale is therefore £34bn and BIS was aiming to raise around £12bn from a five-year sale programme.

It is important to note that the fair value – what the government thinks the loans are worth – is not what will be used in a value for money test. This is because the government uses a much higher discount rate to assess VfM: a sale could represent a substantial loss to government but still go ahead, since a higher discount rate means a lower valuation for future money.

Page 75 of the 2015/16 accounts:

Under accounting policies the amortised cost discount rate (currently 0.7 per cent) applies whereas the Department has agreed with HM Treasury that any decision to retain or sell an asset on the balance sheet the applicable discount rate is the social time discount rate (currently 3.5 per cent). The Department will also explore options to sell Green Investment Bank and the Government’s 33 per cent shareholding in Urenco.

The decision to change the reporting discount rate for student loans has sidestepped the dominant political debates about the sustainability of student finance with a classic accounting move, but this means that a central pillar of HE policy – selling the loans to clear the balance sheet and lower national debt – becomes less ‘presentable’.

Remember that the government only raised £3.3bn from the sale of Royal Mail shares and was thought to have missed out on millions. The government is entertaining an annual process that would generate more losses each year – but it’s hoping no one will pay too much attention.

For illustrative purposes here is a simple cash stream (£10 per year for 10 years) discounted at the two different rates (using RPI of 2.8%). You can see that an asset worth £83 would pass a VFM sale test if someone offered £72.

Click on image to enlarge

(ps this was updated as my original spreadsheet used the old plus 2.2 discount rate rather than the plus 3.5 VfM discount rate)

Trackbacks & Pingbacks