Interest rates & How Not to Write About Student Loans

March RPI, the figure used to determine annual interest rates on student loans, was published this week. It has risen to 3.1% – a near doubling from last year’s 1.6%.

In September, those on old-style mortgage loans will see their interest rise to 3.1% for 2017/18.

Those on loans taken out between 1998 and 2012 benefit from a clause that sets interest at the lower of RPI or bank rates plus 1 percentage point. The bank base rate is currently 0.25% meaning that borrowers with these loans are seeing interest accrue at 1.25%. That base rate is expected to rise in the next 18 months – possibly more than once – as it does so the interest rate on student loans will climb with it. From September, the new RPI figure will set an upper limit on interest in 2017/18 of 3.1% (it will be 1.6% until then). (That is, despite media reports, the base rate today does not fix the interest rate for 2017/18, but the March RPI will set an upper limit for the year).

For student loans issued to those who’ve started an undergraduate course since 2012, there is a different arrangement. Interest rates while studying are RPI plus 3 percentage points, so that will rise to 6.1% for the year starting in September. After a student leaves their course, interest accruing is set by a taper determined by earnings: those earning £21000 per year and under see RPI; those earning £41000 and above see RPI plus 3 percentage points; those earning in between those two points receive a proportionate rate. That means that for 2017/18 there is a sliding scale between 3.1% and 6.1%. (The new postgraduate loans do not have the interest rate taper and borrowers face interest accruing at RPI plus 3 percentage points throughout).

Now for my standard complaint.

Student loaned issued to those starting since 1998 are income contingent repayment loans. This means that comparisons with commercial loans that only look at interest rates are misleading.

With commercial loans, you will be expected to repay the principal borrowed and all of the interest accruing and you will be expected to do so relatively quickly.

Income contingent loans are designed to mimic a proportionate graduate tax: a borrower may not repay the principal, let alone the interest. The government currently commits to writing off any outstanding balance thirty years after repayments fall due. Looking at the interest rate on ICR loans without looking at how that interest translates into repayments is misleading. (It is also important to understand the time value of money as cash amounts paid back in 10 years are not necessarily of lower value than higher cash amounts paid back over 30 to 35 years).

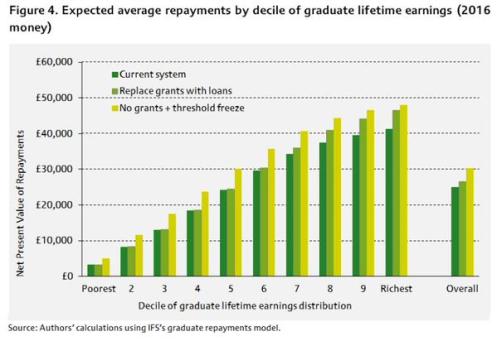

The chart below is from a 2015 Institute of Fiscal Studies report and is a little out-of-date in relation to the current government’s discount rate for student loans, but otherwise it gives a good illustration of the difference in repayments made under the income contingent repayment scheme. Even with graduate debt around £50 000, the net present value of repayments for the majority of borrowers is well below that principal.

All loans should be judged by the value of the repayments demanded. When evaluating commercial loans the interest rate is the good shorthand, but income contingent repayment loans are much more complicated and the repayment threshold of £21 000 lowers repayments and provides the kind of protection to borrowers that is simply absent from commercial loans.

This basic point about income contingent repayment loans is particularly important as commercial lenders – whose repayment conditions will be more onerous and most likely more expensive for everyone other than those who go on to be very high earners – isolate the interest rate comparison and use it to mislead potential borrowers.

It is therefore very disappointing that a Guardian personal finance journalist has churned around a press release from “Save the Student” and made all these mistakes (and more). The article never mentions how income contingent loans work (the brief reference to a repayment threshold doesn’t explain income contingency) and leaves the reader with the suggestion that commercial loans or (re-)mortgaging might be a cheaper way to finance study. They aren’t likely to be: in addition, SLC Student loans have built-in insurance, they are written off in the event of the borrower dying or becoming unable to work through disability.

By all means criticise the cost of English HE – I do – but don’t thereby drive potential students into the arms of commercial lenders and much more onerous debt.