£11 billion of “Supplements” used for loans

Given the relative absence of higher education from yesterday’s Autumn Statement, I turned my attention to the Department for Education’s 2019/20 annual accounts, which were published earlier this month.

Regarding student loans, we have been in something of a hiatus since 2018, when Theresa May announced an review of post-18 funding and commissioned the Augar panel, which reported last summer. Although there were suggestions that we might get a long overdue response to the latter yesterday, we will probably have to wait now until the Budget next March, when the government will hope to have a better sense of its spending commitments.

That leaves student loan finance in limbo with the small, nominal budget allocation for loan write-offs shored up by large “Supplementary Estimates” provided by parliament each February.

This is in spite of an apparent “target RAB” of 36% and a budgeting process hanging over from 2014, when the old department for Business, Innovation and Skills (BIS) had responsibility for loans and was being “incentivised” to reduce the cost of the loan scheme. You can see both of these features still stipulated in the latest Consolidated Budgeting Guidance, but they represent zombie policy with little to no bearing on events.

Why so? Well, DfE was given an extra £12billion plus back in February to supplement 2019/20’s budget for “non-cash RDEL” (mostly student loan “impairments”) of £4.7billion per year. (Student loans are “impaired” because the loans are worth less in estimated repayments than the cash advanced.) The supplement produces a total that is more than triple the original allocation.

And… DfE managed to spend nearly £16billion of that last year. The accounts report an “underspend” of £1.1bn against that total.

As can be seen from the table below, “Fair Value movement” for student loans amounted to a non-cash cost of over £14billion.

£17.6billion of new loans were issued, a net increase of £15billion once repayments of over £2billion are considered, but the new impairments on post-2012 loans increased by £12.3billion; for “pre-2012” loans the stock remaining at year-end lost nearly £1.7bn when revalued.

Although the nominal value (“face value”) of outstanding post-2012 loan balances is nearly £105billion, those loans are thought to be worth less than £50bn.

The increases in impairments break down into a RAB charge and a stock charge.

The RAB charge is the estimated impairment on new loans issued. That came to nearly £9billion, reflecting the latest understanding that only 47% of the £17billion+ of annual undergraduate loan outlay is now expected to be repaid in net present value terms. Ie, the RAB charge is 53%, well above the official target of 36%.

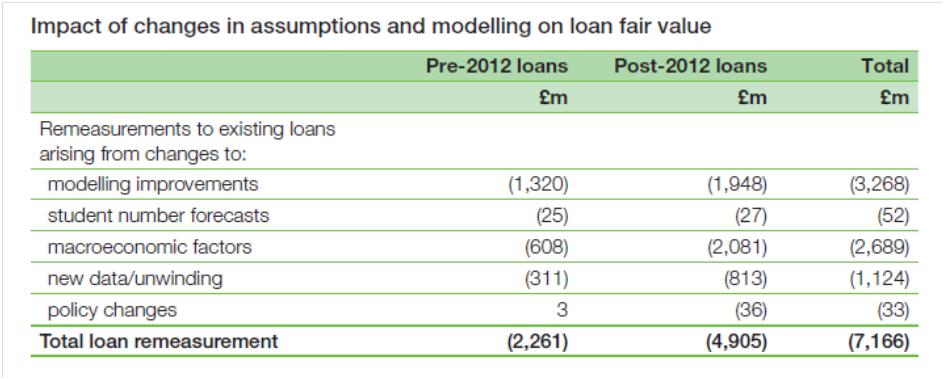

The other £7billion was a write down on loans issued in previous years and is based on changes made to the model used to estimate loan repayments. Only £2.1billion of that downwards revaluation is attributable to Covid (the loans were revalued in July).

The accounts make available a further breakdown of the modelling changes.

The implications seem clear: HE is due a day of reckoning. From a financial perspective, the strongest measures would control outlay rather than boosting repayments. In cash terms, the former has immediate impact on finances, whereas the latter spreads the effect over decades and is politically difficult at this time.

Tuition fees are to be frozen again in 2021/22 and we should expect this to continue. Announcements in FE suggest that the government would also like students to switch away from longer, more expensive HE courses. More radically, I would expect the government to be reviewing the Augar suggestions of tuition fee reductions and caps on places for certain courses (Recommendation 3.7).1

Back at the Conservative Party Conference, Rishi Sunak warned of “hard choices” to come and promised to “balance the books”:

“Over the medium term getting our borrowing and debt back under control. We have a sacred responsibility to future generations to leave the public finances strong, and through careful management of our economy, this Conservative government will always balance the books. If instead we argue there is no limit on what we can spend, that we can simply borrow our way out of any hole, what is the point in us?”

That final question invites some alternative answers, but the Spending Review’s focus on Further Education reinforces the idea that HE will be the required to balance the increased spending on the former.

1 “We therefore invite the government to consider the case for encouraging the OfS to stipulate in exceptional circumstances a limit to the numbers an HEI could enrol on a specific course, or group of courses. It would be critical for the OfS to be transparent about the grounds and process for such an intervention and we can offer no more than a broad indication of what these circumstances might be. Where there is persistent evidence of poor value for students in terms of employment and earnings and for the public in terms of loan repayments, the OfS would have the regulatory authority to place a limit, for a fixed period, on the numbers eligible for financial support who could be admitted to the course. The institution in question would remain free to recruit to all other courses without restriction. Such a cap system would clearly target the institutions that are offering poor value, rather than altering the entry criteria for individual students.”

p. 102, Independent Panel Report to the Review of post-18 Education & Funding

Trackbacks & Pingbacks