IFS on tuition fees

As you’ve probably gathered from the media coverage, the Institute for Fiscal Studies has a new report out on tuition fees in England.

It offers a thorough summary of changes since 2012 and reinforces a number of points made here and elsewhere about the regressive nature of freezing the repayment threshold and how the abolition of maintenance grants plays out.

IFS even conclude with an oblique critique of the current system suggesting that government needs to increase its long-run contribution and be less focused on deficit reduction in this regard. In effect, IFS indicates that the cost of HE may now be too high and that this high cost ‘may reduce participation in the long-run’. This is awkward for Jo Johnson, who has spent the last few days using IFS findings to rebut Damien Green and the Labour pledge to abolish tuition fees.

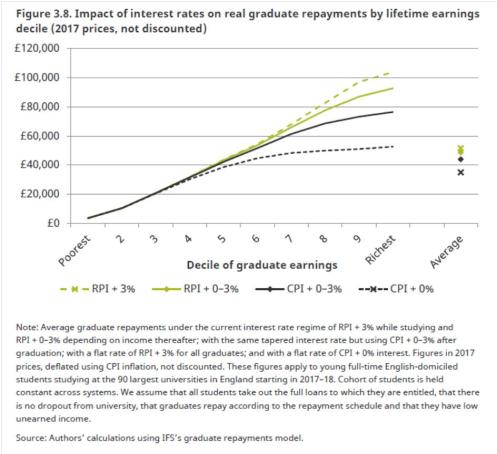

The government is likely to review the interest rates, since these are scheduled to increase in September to a range of 3.1 to 6.1 per cent (based on March’s RPI figure of 3.1%). These figures were used by IFS in its analysis and underpin large increases in contributions made by the highest earners, such that the top-earning 30% of borrowers are now modelled to return a surplus of repayments to the government (the negative ‘RAB charge’ in the IFS chart below, where the resource accounting and budgeting charge represents the resource implications for the Department for Education, who now own the loans).

Politically a retreat from these high figures is probably in the government’s interest, but as IFS show, a reduction in interest rates would be regressive in that it would only benefit higher earners.

(Note that the figures in this chart are ‘deflated’ to 2017 equivalents using CPI and so differ markedly from figures showing the cost to government based on the government’s discount rate of RPI + 0.7%).

IFS describe the high interest rates and ‘negative RABs’ as a risk to government, since if high earners find an alternative way to finance their study then their cross-subsidy is removed and the scheme becomes more expensive.

I’m not convinced the Treasury sees it so straightforwardly.

The government has in the past considered schemes to encourage early, voluntary repayment of loans (which would similarly allow individuals to escape the effects of real interest). In fact, current policy explicitly expresses its preference for cash today at the expense of long run loss: the sale of student loans is emblematic here. If fewer people borrow in the first place or more repay early, then, all else being equal, public sector net debt is reduced in the short run.

The IFS insist that such measures do not improve the public finances – and they are right – but they improve key public finance statistics, like PSND, and politically this presentation matters. After all, what is the fiscal mandate other than an appeal to the public: judge us against these targets! and having PSND fall as a percentage of GDP is one of those targets.

On the flip side, but not noted by IFS, the Department for Education has been set a ‘target RAB’ of 28 per cent by the Treasury. For 2015/16, the RAB charge was well under that at 23%, but this was due to rise last financial year with the impact of maintenance changes; it will rise again in 2017/18 as higher tuition fees arrive. Should the official RAB charge rise above the target, then a special budgeting procedure kicks in which would see DfE having to make savings elsewhere in its budget. (DfE has a much bigger budget than BIS did, so the incentives behind the new budgeting procedure may have less effect now.)

The IFS have assessed the RAB charge on the 2017/18 cohort to be 31%. This indicates that there may be pressure on the DfE budget, which as such would feature in discussions around changes to the interest rate. (We should note the official RAB is not calculated per cohort, but on each year’s loan issue and therefore covers students in more than one cohort).

For all the official reassurance around the English fee-loan regime, the number of tweaks to policy, loan terms and accounting / budgeting conventions is indicative of an experiment that is still in its early phases. It is also worth remembering that recent rapid rises in RPI will have caused significant downwards revisions to the value of existing loans and that last August’s decision by the Bank of England to lower base rates to 0.25% has similarly damaged the value of pre-2012 loans. In February, DfE bid for £11billion in supplementary resource to cover ‘movements in the macroeconomic determinants’ underpinning the value of the loan book’.

Further finagling of the system may be insufficient at a time when public goodwill seems to have moved decisively against the basic features of the scheme.

https://www.independent.co.uk/news/uk/politics/student-loan-interest-rate-hike-u-turn-andrea-leadsom-minister-education-department-university-a7827381.html%3Famp

It is interesting to note that the rate on post-2012 student loans has already been higher than the scheduled 6.1% for September. It was 6.6% in 2012/13 and 6.3% the following year but the accumulated debt it was levied on was of course lower then due to those being the first two years of the post-2012 system and maintenance grants reducing the total debt accessible.

It’s postgraduate loans where the biggest difference for most would be felt from a change to the RPI + 3% formula as this would benefit lower earners as well as higher earners due to the smaller loan balance.

But if the DfE are to change the formula for this September they need to get a move on as it would require the current regulations to be amended and the statutory instrument would have to be laid before the summer recess on 20th July for it to take effect in September.

Under the current regulations the only alternative to setting interest on post-2012 loans and postgrad loans at RPI + 3% is to not set a rate at all “If the Authority determines that post-2012 loans will bear interest…”

http://www.legislation.gov.uk/uksi/2012/1309/regulation/10/made

http://www.legislation.gov.uk/uksi/2016/606/regulation/31/made

Yes – you’re right. I’ve no truck with postgraduate loans – the money made available should have gone into improving undergraduate terms. The interest rate coupled with the 15% repayment rate for those with UG and PG loans is likely to prove expensive for borrowers.

https://www.thetimes.co.uk/edition/news/frankenstein-tuition-fees-to-be-reviewed-mnksjmbxw

Looking like something’s going to change with the interest rate.

“Sources close to Jo Johnson, the universities minister, indicated this weekend that a looming interest rate rise on student loans to 6.1% might be reduced and also said a review of higher education funding was promised in the Tory manifesto. Johnson indicated last week that the situation was being looked at.”

Or not.

https://www.thetimes.co.uk/article/student-loans-not-as-bad-as-wonga-insist-ministers-vqzbdx690

The interest rate should be structured in such a way that when inflation is ‘average’ (which for RPI should be around 2.5-3%) the average borrower’s repayments should be able to at least eat into the capital.

It’s ridiculous to have a situation where the average borrower has a £50,000 balance on graduation and with RPI at 3%, no-one earning between £21,000 and £41,000 can eat into the capital as interest applied at £41,000 salary is £3,000 (6% x £50,000) whereas repayments are only 9% x (£41,000 – £21,000 = £20,000) = £1,800.

On a salary of £31,000 and interest applied at 4.5%, the same is true:

repayments are 9% of the £10,000 earned above £21,000 = £900 but interest applied is £2,250.

The only chance anyone has of eating into the capital is if RPI is low. It’s ridiculous.

Changing to CPI would help but the interest rate needs reforming. It can be reformed while remaining progressive.