Fiscal illusions & student loan interest

I have tended to neglect the impact of student loans on measures of the “deficit”, whether Public Sector Net Borrowing, the Current Balance or whatever. In this context, the deficit measures the amount by which public sector spending (explained here by the Office for National Statistics) exceeds income (taxes and the like).

My neglect was premised on the basic point that student loan outlay (new lending) and annual repayments (from borrowers) are classed as ‘financial transactions’ and are therefore not scored as expenditure or income in this way. They are outside “the deficit”. They do though require cash to cover the annual shortfall between outlay and repayments and this makes its way through to Public Sector Net Debt. I have then tended to focus on the cash impacts and how they bear upon PSND. (Note that this nuance in accounting leads people to mistake student loans as being somehow off-balance-sheet. They are on the national balance sheet they just don’t score as you would expect in the normal headline fiscal statistics).

These accounting quirks are one of the main attractions of student loans to politicians. You can reduce the “deficit” dramatically by switching from expenditure (e.g. on tuition or maintenance grants) to loans. The whole cash outlay disappears from expenditure regardless of the amount you expect to get back from loans. It looks like you are doing more with less.

However, elements of student loans do score against income and expenditure: interest receivable scores as income each year and the face value of outstanding loan balances scores as expenditure when such write-offs occur (and loan accounts are therefore closed). For a single set of loans, the net effect of this set of transactions is to record the cash loss or surplus generated.

This might be a bit surprising but it is based on the following accounting identity:

(1) Loan Outlay + Interest Accrued = Outstanding Balance + Repayments

A little algebraic manipulation tells us that when repayments are less than outlay:

(2) Loan Outlay – Repayments = Outstanding Balance – Interest Accrued

Since Loan Outlay – Repayments is defines our loss, we can also capture it with the right-hand side of our equation (2) above.

That is, loan outlay and repayments are never recorded directly in the deficit. Loss is captured by recording Interest Accruing each year as a benefit and then charging the outstanding balance as expenditure at the end.

There are three consequences to this:

- Interest Accruing is recorded – but this is Interest Receivable not any measure of interest repayments. It is also non-cash.

- Timings matter. The deficit benefits from the Interest Accruing for the whole lifetime of the loans (a maximum of 30-35 years for new loans) until at the end the deficit takes the negative hit and undoes those years of benefit!

- Write-offs are also non-cash – they are simply recording the effects of the financial transactions once they are finalised. Loans went out the door and repayments came back in previous periods. (Write-offs count as capital expenditure and do not score in the Current Balance).

You might then conclude (like I did) that it’s better not to look at deficit measures when thinking about loans and instead concentrate on the impact on cash and debt and on the departmental accounts (which are run on an accruals basis, not on cash in, cash out). Indeed the Office for Budgetary Responsibility identified this student loan interest as a ‘fiscal illlusion’ in its most recent report.

I think that neglect is a mistake. We need to consider all of these fiscal and budgetary aspects and impacts. If only, because post-2012 loans run with real rates of interest (for graduates and university leavers, 3.1% to 6.1% from September; current students will see 6.1%). These real rates exceed the cost of servicing any borrowing used to create student loans in the first place.

Here are the OBR’s projections for Interest Receivable over the next five years:

|

2017/18 |

2018/19 |

2019/20 |

2020/21 |

2021/22 |

|

| Interest Receivable (£billions) |

3.0 |

4.5 |

5.5 |

6.2 |

7.1 |

That’s a substantial impact on PSNB (and the Current Balance) when you consider that the current government is aiming to eliminate the deficit.

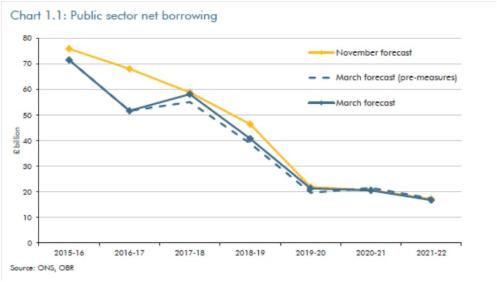

Here is the OBR’s March 2017 projection for PSNB:

With that to mind, it is perhaps no surprise that the Conservatives have chosen not to review current interest rates on student loans. (Though I think there are other budgetary considerations at play).

Governments have their main fiscal statistic “flattered” for decades after the introduction of higher loans with real interest rates. We won’t see the first substantial policy write-offs until the 2040s. (Loans are also written off annually in the event of death or disability but these unfortunate events affect only a very small number of loan accounts). Unfortunately, at that point it’s not as if the illusion will be pricked – you will have one year of loan write-offs set against the interest accruing against three decades and more of loan accounts!

A more general lesson follows: it’s a mistake to talk about “the deficit” and “the debt” without some awareness the composition and interrelation of those headline statistics (let alone what they mean for the state of the economy more generally). Student loans represent a very particular case of what Simon Wren-Lewis calls “mediamacro”, as that is characterised by a focus on reducing the deficit.

Now that student loans are so sizeable it may make sense to develop new ways of capturing the fiscal position. So long as loans are loss-making and so long-lived, it makes little sense to include interest receivable (but likely never to be received) as income.

Trackbacks & Pingbacks