Fiscal Distortions – rolling loan cohorts & national account implications

I have in a previous post explained the basic presentational advantages accorded to student loans under national accounting conventions. In particular, a graduate tax with identical cashflows and therefore long-run costs would have a completely different impact on the deficit measure, which the government targets in its fiscal mandate.

Because a loan creates an asset (money owed to government), interest accruing against the outstanding balance counts as income (though it is receivable, not received) and write-offs, when they occur, count as capital expenditure. The net effect – the difference between the two – equates to the loss (or surplus) made on the loans issued for a particular cohort.

For a graduate tax, there is no asset, only a policy, and so a graduate tax cannot exploit the conventions governing loans as “financial transactions”. For that identically costing graduate tax, annual outlay counts as current expenditure and repayments count as income.

As explained before, the timings therefore flatter the student loan scheme: Annual Interest Accrued is recorded as income every year and the expenditure item occurs only at the end, when accounts are closed and balances written off.

For the graduate tax, the opposite happens: expenditure is recorded first and then gradually undone by payments coming in.

If you suffer from deficit fetishism, or just opportunism, then this rules out a graduate tax.

I have explained this before. It forms part of what the Office for Budgetary Responsibility calls a ‘fiscal illusion’. (In its most recent Economic & Fiscal Outlook, OBR again complained that the treatment of student loan interest ‘does not reflect fiscal reality’.)

The problem arises because here the government exploits international accounting conventions on loans. They are designed for loans which are repaid in full and in particular loans where periodic repayments at least match interest accruing. The conventions were not designed to cope with income contingent repayment loans with large subsidies.

As a result, the Treasury Committee has asked the Office for National Statistics to review the accounting treatment for student loans:

The Government is not responsible for the international accounting rules that allow the fiscal illusions within student loans to exist. However, the National Accounts accounting rules regarding financial transactions were not intended to be used for loans that, as the Government readily promotes, are designed to not be paid back in full. Loans that are intended to be written off are, in substance, a partially repayable grant rather than a loan. The ONS should re-examine its classification of student loans as financial assets—which they are in legal form—and consider whether a portion of the loan should, in substance, be classed as a grant.

Paragraph 31, Student Loans

Here, I want to underscore two further points using OBR figures.

The first is: the usual focus on the deficit is misplaced for student loans. The standard narrative is that reducing the deficit (the difference between income and expenditure) reduces the amount of annual borrowing that needs to be done and so slows down the rate of growth of debt as measured by Public Sector Net Debt.

But the deficit is not the driver of debt here – the Public Sector Net Cash Requirement is. Loan Outlay may be excluded from the deficit but it has to be added back in to get from Public Sector Net Borrowing (the deficit) to PSNCR.

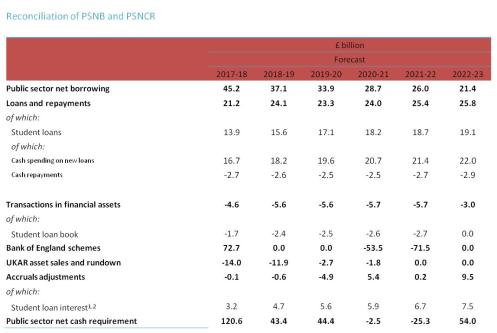

The table below (adapted from the OBR’s latest Economic & Fiscal Outlook) shows how that happens. “Cash spending on new loans” is estimated to be £16.7bn (for the whole of the UK) this year, climbing to £22bn by 2022-23. The shortfall between that cash and cash received as repayments has to be financed – it doesn’t trouble the deficit.

You can also see that student loan interest has to be removed to avoid double-counting and that interest accruing (recorded as income for the purposes of the deficit) is always greater than actual repayments received. In 2022-23, Interest Accrued will be £7.5bn, but repayments less than £3bn!

So, in sum, arguing about whether to have a graduate tax or a student loan scheme from an accounting position is really arguing about whether to place the cash spending and cash repayments under “Public Sector Net Borrowing” (first row) or in a subsequent row. That is, you are only really debating how to classify it, not dealing with concrete fiscal differences.

But the deficit is the target the government presents to the public, so it looks better if it is smaller. That £3.2bn in student loan interest for 2017/18 has helped the government declare that it has eliminated its current balance deficit. (The current balance is the difference between income and current expenditure). In fact, it appears to have made all the difference, as the surplus from Jan 17 to Jan 18 is £3bn.

The second point is that the fiscal illusions are magnified when you project forward a few decades to the point where the loan scheme is at maturity in accounting terms (you have 30 years of graduate borrowers). For an explanation of the accounting identity involved here see this post.

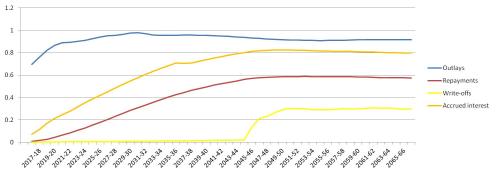

The table below is produced from data accompanying the OBR’s January 2017 Fiscal Sustainability Report. The figures will need to be revised to reflect October’s decision to raise the repayment threshold, but the chart serves to illustrate the accounting problems quite nicely.

Fiscal impacts as per cent of GDP (GDP is currently around £2 000 billion)

Loan Outlays are in blue, Repayments in red. Repayments are always below outlay, even though repayments are from all open accounts and outlay is the annual cash used to issue new loans.

Loans are subsidised: the government loses money on loans and treating outlay as expenditure and repayments as income would show that up well after 2045, once the gap between blue and red has stabilised.

The difference between the two each year is what would show up in the deficit if you had the graduate tax. Governments are concerned about the shortfall in the early years, but as the table above shows – that shortfall has to be made up with borrowing anyway when using loans.

Now look at Accrued Interest in Orange and Write-Offs in yellow. This is what scores in the deficit for loans.

Note that Accrued Interest (Income) is not only above repayments, but always above write-offs (expenditure). The relationship between what is scored as income and what is scored as expenditure has been reversed because of the timing differences. “Income” is always greater than “expenditure”.

This means that the current national accounting treatment misrepresents student loans as surplus generating because they benefit the deficit measure.

In sum:

- the accounting treatment for “financial transactions” is not rigorous when applied to student loans: it was not designed for loss-making loans nor for income contingent repayment loans;

- moreover, the deficit treatment distorts and obscures the costs of loans; going so far to show them as surplus-generating when they need to be subsidised.

No good can come from having an accounting system that doesn’t capture accurately the effects of policy decisions. It’s worse if such distortions are presented as a virtue of student loans. Above all, it’s a problem if alternative policies are being excluded from consideration because of how they would be classified differently in terms of income and expenditure.

You could simply ignore the deficit fundamentalists and focus instead on PSNCR and debt pathways for student loans, but the Treasury Committee is right to call on the ONS to review the current treatment.

On a similar note, the ONS has still not decided how to categorise December’s student loan securitisation. That would determine whether sold loans ever appear as an expenditure item at all – the interpretation the government is seeking would be contrary to the basic principles of public sector accounting.

Trackbacks & Pingbacks