October 2018 Budget – OBR continues its accounting commentary

Since we are awaiting the outcome of the Office for National Statistics review into student loan accounting and the government review of tertiary education, expectations for HE announcements in today’s Budget weren’t high.

In the end I only spotted two relevant to this blog:

- the maximum level for undergraduate tuition fees will be frozen at £9,250 pa in 2019/20 (though OBR expects them to rise in line with inflation thereafter);

- the government announced an additional year for its current plan of selling pre-2012 student loans, with the expectation that £3billion will be raised in 2022/23. This brings the planned total revenue to circa £15billion (£1.7bn was raised in last year’s sale, a second sale is expected to conclude in December). Philip Hammond decision to end the nonsense of PFI schemes hasn’t extended to this policy that also makes long-run losses for presentational gains.

Of more interest is that the Office for Budgetary Responsibility, in its accompanying Economic & Fiscal Outlook, chose to continue its commentary on the perversity of the accounting treatment of student loans and their sale.

Two new “boxes” in its regular report gave pithy summaries of the problems and the likely impact of the ONS review.

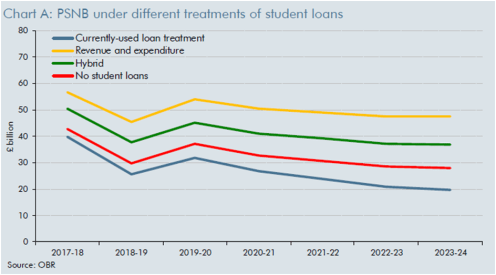

Box 4.3 included the chart below which shows how the current figure (in blue) for Public Sector Net Borrowing (“the deficit”) would be changed by two contrasting approaches: treating student loan outlay as expenditure and loan repayments as income (the graduate tax model) in yellow; or a hybrid approach (green) that treats student loans as a mixture of loan (the part repaid) and grants (the part written off). Even the second would add £10billion per year this year to PSNB.

Note that the interest illusion on student loans (interest accruing is booked as income even though it might not be received) means that not issuing loans at all worsens PSNB over the forecast period, even though loans are subsidised.

OBR has previously indicated a preference for the “hybrid treatment”. It concludes:

The difference between the current treatment and our estimate of the hybrid treatment illustrates the extent of the fiscal illusion created by the current approach. It suggests the current treatment flatters the deficit by £12.3 billion in 2018-19 and £17.1 billion in 2023-24. In the Government’s fiscal target year of 2020-21, the difference is £14.4 billion – just less than the margin by which it is set to meet its self-imposed ‘fiscal mandate’. (my emphasis in bold)

My own view is that the ONS is unlikely to recommend the “hybrid treatment” or the “revenue / expenditure” approach. The most likely outcome will be that the “interest illusion” will be removed in isolation. That will affect PSNB, but not by as much as the options shown above.

OBR also provides the relevant figures to calculate an impact focused solely on accrued interest (Table 4.36):

Removing these amounts from government income still has a substantial impact on PSNB:

This would undermine Hammond’s claim today to have met his targets three years early. From his speech today:

Borrowing this year will be £11.6bn lower than forecast at the Spring Statement… just 1.2% of GDP…and is then set to fall from £31.8bn in 2019/20…

…to £26.7bn in 2020-21…

…£23.8bn in ‘21’-‘22’…

…£20.8bn in ’22-‘23’

…and £19.8bn in 2023-24, its lowest level in over 20 years…

We meet our structural borrowing target 3 years early and deliver borrowing of just 1.3% of GDP in 20-21 maintaining £15.4bn headroom against our 2% Fiscal Rules target. … Both our fiscal rules met; both of them three years early. So, Mr Deputy Speaker, Fiscal Phil says: Fiscal Rules OK.

It remains to be seen how the Fiscal Rules Rule once the ONS report in December. (Apologies for the formatting above but “Ellipses rule OK” for Punchline Phil too.)