May’s largesse costed & the end of RAB?

Last week, the Department for Education (DfE) published its financial report and annual statement for the year ending 31 March 2018.

With regard to “English” student loans, it confirmed one thing we already know: December’s securitisation of the first tranche of income contingent repayment loans meant a loss of £900m had to be booked. The loans sold were worth £2.6bn; the government received £1.7bn. DfE had received assurances that this would not affect its budgets. As we saw the week before last, the National Audit Office had some criticisms: chiefly that the aim to reduce PSND was leading to losses that the government was assessing inconsistently.

In the absence of further announcements from government, the DfE accounts provide one nugget of new information about the sale programme, which was originally meant to raise £12bn in cash over five years. It appears that these prospects have dimmed as we are offered a new range: ” The loan sale programme aims to generate between £9.2 billion and £12 billion in proceeds by 2021-22″ (p. 8). This revision was not communicated to the Office for Budgetary Responsibility: the latest edition of their long-range Fiscal Sustainability Report, published annually, appeared in June and still based its projections on the £12bn figure.

The second piece of news is that we have an official estimate of the cost of Theresa May’s decision to raise the repayment threshold from £21,000 to £25,000 in April.

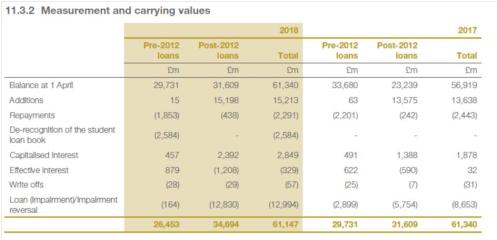

The existing stock of “post-2012 loans”, worth £31.6bn at the start of the year, lost £5.346billion in value as a result.

The loan book now has a face value of £102bn, but is still only worth £61bn.

In fact, the “carrying value” of all outstanding loans went down last year, despite £15bn of new loans being issued. Against that outlay, repayments (£2.3bn) and “de-recognised” loans (the £2.6bn sold) were still small amounts.

On top of the losses for existing loans, the new loans were “impaired” by £6.6bn, meaning that DfE only expects to get the equivalent back of £8.4bn in repayments on that £15bn.

DfE, 201718 Financial Statement

DfE, 201718 Financial Statement

The “RAB charge” was as a percentage was then slightly under 45%. But the sum needed was well above the original £3.5bn DfE RAB allocation for 2016/17. In effect, May’s decision has added £3bn to the long-run cost of this year’s tranche of loans. As annual loan issuance is expected to increase, this cost will also go up.

Back in February, DfE was given a “supplement” of £14.7bn for this year to cover the change in loan value resulting from May’s pledge. In the end, only about £9.4bn of it was utilised and so DfE can record an “underspend” of £5.3billion in its accounts.

It’s not clear what will happen in future. DfE still has its old RAB allocations for the next two years: £3.9bn for 2018/19 and £4.3bn for the year after. It both cases these are premised on a RAB of under 25%. The chancellor chose not to alter these at the last Budget and may be waiting for the outcome of the review of tertiary education before acting.

There was one further important development. The implementation of new accounting standards for “financial instruments” will affect the way loans are presented in departmental accounts. This will take effect in this new financial year and is separate to the national accounting issue. In both cases though, student loans are recognised to be sufficiently un-loanlike to require a changed treatment. In this case, the DfE has announced that the problem resides with repayments.

Under IFRS 9 Financial Instruments (IFRS 9), loans must be such that their cashflows are generated “solely [by] payments of principal and interest”. As we know, for income contingent loans, repayments are determined primarily by income.

The annual statement contains the following paragraph:

The loans’ contractual cash flows do not meet the standard’s definition of being solely payments of principal and interest (SPPI), and therefore the loans cannot continue to be measured on an amortised cost basis. The Department considers the SPPI test to be failed because the terms of student loans do not generate cash flows designed to fully recover interest and principle[sic]. Student loans are issued to support students and the Higher and Further Education sectors without credit checks, and the loans are forgiven after an agreed period and under other circumstances. (p. 128, my emphasis in bold)

DfE expects the value of loans to reduce as a result of this change, which will involve trying to implement a “fair value” measure primarily designed to reflect the market value of assets.

This may herald the end of RAB as we have known it. Certainly there will no longer be a separate “impairment” built up out of such charges.

It should be noted that a significant difference in the presentation of the loan book, when compared to the presentation under IAS 39, is that loan additions will be shown net of any fair value adjustment, rather than showing separately the additions and RAB charge as per the current treatment. This in turn will result in a lower figure being presented going forward for both additions and in year revaluation … . (my emphasis in bold).

Trackbacks & Pingbacks