PAC report on student loan sale: some conceptual errors

The Public Accounts Committee report into the sale of student loans garnered some good headlines today and contained some good quotes, but in truth it failed to get at the real issues around the securitisation and made some odd errors. People interested should go back to the National Audit Office report or my own writing (a new, “long read” article will hopefully be out shortly).

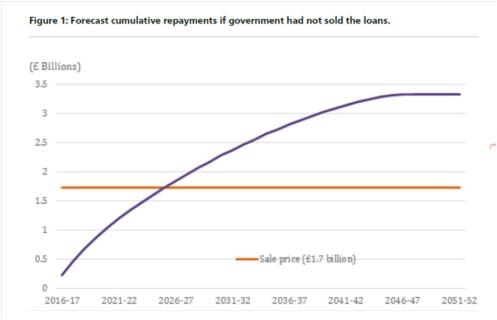

PAC’s confusion can be summed up with the one chart it provides in the report.

The line in blue shows cumulative, cash repayments representing the income stream associated with the loans sold.

Unfortunately, you can’t use simple cash figures to decide whether the sale price of £1.7bn was too high or too low. The value of cash is not stable. £1 today is not worth the same as £1 next year or £1 in 2026 or 2045.

When PAC claims that the sale price could have been recouped within eight years it is demonstrating its fundamental confusion. £1.7bn received today is not the same as £1.7bn received over the next eight years. Instead the government has to make a decision about how to “discount” future income received to translate it into today’s equivalent. This is known as a “present value” calculation. You can see that a number of factors come in to play: inflation and the reliability of repayment being the main ones.

These factors get wrapped up into a “discount rate”, giving me the means to translate a future cash payment into an equivalent value today. If I adopt a discount rate of 5%, I am saying that I think that £1 today is equivalent to £1.05 received in a years’ time, £1.10 in two, £1.16 in three, £1.28 in five etc. The calculation is analogous to calculating compound interest.

The government sold student loans at a loss – that’s not in dispute. But what PAC has confused is that the loss is determined by government’s decision to use two different discount rates: one to record the value of loans in the Department for Education’s accounts (loans are on the balance sheet!) and another to determine what price it would accept on the sale.

The financial reporting rate used by DfE is RPI plus 0.7%; the “retention value” rate used to determine a price is RPI plus … well somewhere between 2.5% and 3.5% – the exact rate is “commercially confidential”. You can see though that the difference in rates is substantial and a higher discount rate puts a lower value on future money. With a discount rate of 6% I would sell the promise of £1.05 for less than £1.

Since it doesn’t demonstrate an understanding of discounting, PAC gets confused as to how the sale could be de-risking. Once you have discounted the cashflow, you have to wait much longer to get repayments equivalent to £1.7bn today. The longer you wait, the more likely it is that actual repayments diverge from those projected in 2017.

What PAC should have concentrated one here is how the government justifies using two different rates and whether the higher rate is at all appropriate in this case. The higher rate is based on the “social time preference time rate” (STPR), which has been unchanged since 2006, despite dramatic reductions in the government’s cost of borrowing (circa 1.6% at the time of the sale last December, but closer to 2% now – that is, below RPI).

When PAC does discuss the STPR, its brevity is unhelpful.

p. 12 paragraph 17:

Government works on the assumption that if the money is not tied up in an asset it can be reinvested at return equal to or greater than the STPR … . This rate is significantly higher than market risk free interest rate of 1.6% and therefore meant that government’s retention value was lower than: what investors were likely to pay, how the Department valued the loans in its accounts, and the other valuations the Department calculated. It also demonstrates the impact of government’s stated counterfactual: to think about the return which could be made by utilising the money raised from selling student loans, rather than borrow more money. In effect, government does not consider borrowing more money at 1.6%, but pays a return of 6.5% to the private sector for £1.7 billion (see above) as government believes it can reinvest this money and get a return of at the very least 5.5%. (my emphasis)

The STPR is meant to express “the public’s” preference for cash today over the returns associated with assets and investment. It is sometimes called the “hurdle rate” as infrastructure projects have to demonstrate that the associated future benefits outweigh the costs today using this discount rate.

In this particular case, the public’s preference for having a lower Public Sector Net Debt figure is meant to justify using the higher rate. Asset sale programmes are aimed at reducing debt, despite what Jonathan Slater, permanent secretary to DfE, told the committee in September. I include a rather long passage from his evidence to illuminate PAC’s summary:

Thirdly and finally, when we are working out what Charles [Roxburgh] rightly calls the retention value—what it is worth to keep the thing—the alternative, in this context as opposed to accounting, is not borrowing more. That is not an alternative at this point because the way the Government does it is to set its overall fiscal strategy on the basis of a certain level of borrowing, as you know; it sets its targets for borrowing. If we were not to sell the student loan book, we would not have the opportunity to borrow more.

What would we be doing? We would be spending less. The whole point of selling the student loan book is to enable you to spend things without increasing debt or taxing more. That is the whole point of it.

When we consider the alternative—this is the last bit, I promise—what would it be? It would not be borrowing more, so we do not use a borrowing interest rate. The alternative would be not spending the money. What we do to calculate the retention value is to say, “Okay, if we do get the money in from the student loan sale, we could spend it on roads, schools, hospitals or whatever, and they would generate a rate of return for us. How much of a rate of return? It would be 2.5% plus RPI, because that is the amount the Treasury requires as a rate of return before it will let me spend anything on a school.” That is the calculation I am doing. If I get the money now, Government can spend it on something with at least 2.5% plus RPI, so as long as the discount I am paying is not more than that, it is value for money.

It all rests, critically, upon the fact that Government cannot increase its level of borrowing. It has set a policy framework that sets it as it is. That is why it is different from borrowing the way you do in the accounts, because that allows borrowing.

Slater is not an expert and what he is trying to explain is that the decision to sell loans is seen through this investment frame. The government though has been explicit that the aim of asset sales is to bring down debt; there is no investment programme to which the £1.7bn is being funnelled. And as the reference to schools, hospitals, roads makes clear, we shouldn’t be left with the impression that the government thinks it has an alternative financial investment which is going to deliver more cash than the loan repayments.

It is a shame that PAC didn’t try to shed some light on the STPR discount rate as it really is central to government policy. That is so high doesn’t just mean that loans are sold cheaply, but that too many infrastructure and investment projects are rejected.