Lowering interest rates – why it’s essential

The Sunday Times reports today that the independent Augar review may recommend lowering interest rates on post-2012 student loans from RPI plus 0-3 percentage points to something akin to that accruing against older loans (the lower of RPI or bank base rates plus 1 pp).

Amongst a raft of other measures, I single this one out not just because its political appeal is obvious, but because it connects with the last post on the Money Saving Expert and Russell Group proposals for reforming the annual student loan statement.

What MSE/RG desire can only be solved by reducing the complexity of loans, not by presentational tweaks. Even though reducing interest rates only benefits higher earners in terms of reducing repayments, the public benefit of simplification trumps that redistributive element of the current scheme. Our current regime’s complications have a propensity to lead people into confusion that engenders harmful financial decisions: making voluntary additional repayments or paying upfront.

Setting aside broader questions about the funding of HE, it is better to forego some repayments from higher earners in order to avoid the potential to lead all borrowers astray.

Finance OhOhOh

What does it mean to say that 75% or 80% won’t repay their student loans before the policy write-off kicks in?

The phrase is a more than a little ambiguous. Strictly speaking it means that over three quarters of borrowers won’t clear their balances. It doesn’t mean that those former students won’t pay out cash amounting to more than the balance they had on leaving university. That is, total repayments are in many cases likely to exceed what was lent to borrowers.

A difficulty then arises: the value of cash is not stable. £1 today is not going to be worth the same as £1 in 2045. How do you compare the value of a cash stream paid out over 30 years with an outstanding balance shown today?

Most people want to know this, because they want to consider whether making additional voluntary loan repayments will save them money in the long run. A thought that arises naturally when looking at the interest rate in isolation.

Some might have the means to pay off their loan balances in full. For certain individuals, this will be a sensible decision: particularly in the case of Postgraduate loans, whose fixed interest of RPI + 3% is likely to punish borrowers who do not repay what they have borrowed quickly (the interest rate combines poorly with concurrent repayment, a low starting debt and a lower repayment threshold).

I start in this way, because this issue is ignored by MSE/RG, who have instead focused solely on reassuring those borrowers whose repayments are projected to be lower than the remaining balance on their account. Quite rightly, they want to advise that group that they should not make additional payments. Unfortunately, they bungle their approach and in doing so leave borrowers with a mess of information and mis-information.

Low Estimates

It is important to stress that in their statement and accompanying report MSE/RG only use one toy example to demonstrate their new statement. And that means what they are suggesting cannot be relied upon.

The example:

A new graduate earning £35,000 has made one year’s worth of repayments in 2018/19. At the repayment threshold of £25,000 that generates a total annual payment of £900. The statement shows the outstanding balance (£50,422) and its movement over the past year (though this is relegated to Page 2). More prominence is given to the final payment date of April 2048. A third and final page outlines “Predictions of your likely future contributions”. It is here that problems arise.

Firstly, a more prominent display for the final repayment date and potential point of write-off is welcome. I’d also like to see a reminder that student loans have another feature absent from commercial loans: death and disability insurance. Parents who remortgage to pay their children’s education upfront have no such protection.

Secondly, the statement imports most of the problems bedevilling the various online calculators available. It contains no caveats about how these figures might differ for men or women or for those from different ethnic backgrounds. I previously forced the Student Loan Company to take down its calculator for assuming all graduates were men.

Thirdly, and most importantly, the statement uses a set of assumptions that are likely to produce much lower estimates of repayments than found in official government loan models or in those operated by London Economics and Institute for Fiscal Studies.

Crucially, MSE/RG make the mistaken assumption that the Bank of England targets the same inflation rate used to calculate the interest accruing against student loans . But the BoE targets CPI, while RPI is used for the loans: CPI is typically significantly lower than RPI, which is no longer classed as an official statistic. Then they assume that average earnings will increase by the current rate of 2.7% for the next 30 years; most other models assume a return to a rate over 4% in the next decade. And they decide the earnings will only increase in line with this rate: that is, no graduate-specific rate, no promotions or positive job changes, and no periods out of work. All this means that projected earnings are dampened and so are repayments.

It is probably because the model lowballs repayments, that MSE/RG have missed the problems I have already outlined. Their example borrower is expected to repay a further £39,000 in total by 2048. On models used by IFS and London Economics, a graduate on a starting salary of £35,000 would be expected to repay much more than that in cash terms and crucially, much more than the £50,000 outstanding balance.

What appears to be a pedantic criticism in fact gets at a crucial conceptual problem. If the MSE/RG only use one such example – a high earner who still repays less than they borrowed – then it is no surprise that they completely ignore the most difficult issue:

What should a borrower do if Page 3 of their statement shows that their expected cash repayments are above the outstanding balance?

Should they look to see if they can pay it off?

What are future repayments worth?

Here’s where the murky topic of present value and discounting forces itself to the fore. How do we adjust the total repayments (£39,000 in this case) made over 30 years (so made at different times) into a figure that makes sense as an equivalent to a cash sum today?

Unfortunately, here MSE/RG drop a clanger.

In attempting to turn that estimated total into “today’s money”, they have made a mathematical mistake and ended up treating the £39,000 as if it were a lump sum paid in 2048. They have inflation-adjusted by dividing £39,000 by 1.02 (their assumed 2%) twenty-nine times (1.02 to the power of 29). That gives you the £22,000. In symbolic form:

£39,000/(1.0229) = £22,000

Think of this as a compound interest problem in reverse. If you put £22,000 into a savings account that gave you 2% per year (paid once per year) you would get roughly £39,000 by 2048.

But that’s not what we should be doing!

The £39,000 isn’t a lump sum paid 29 years in the future. Some payments go out this year, and so shouldn’t be discounted at all. Those paid out 10 years away should only be divided by 1.0210, those in twenty years by 1.0220, and so on. By reproducing the first set of figures used by MSE/RG, I calculate that their “today’s money” equivalent should instead be closer to £29,000 than £22,000.

So in short, MSE/RG underestimate likely repayments (partly by intention, partly by mistake) and then really muck up a present value problem to leave the “today’s money” equivalent lower again. (Note that there is a more technical problem with MSE/RG’s choice to use inflation as the discount rate: this is very unlikely to be appropriate for individuals. A more sensible discount rate might move the “today’s money” equivalent figure to something more reasonable, but it doesn’t change the fact that MSE/RG are suffering from some basic conceptual confusions here.)

The net effect will be to reassure lower earners that they shouldn’t look to make additional repayments, which will only cost them more. But in doing so they underestimate the future repayments of all borrowers and therefore mislead them about their financial position.

According to London Economics, a male graduate with a starting salary of £35,000 would start in the top decile, in fact the top few percentiles of recent graduates. Contra to MSE/RG’s toy model, a top decile male is likely to repay the loan entirely before the write-off. They are likely to make cash repayments of close to £100,000 and repay significantly more in present value terms than what they were loaned.

My point here is not to emphasise how badly that higher earner is served by MSE/RG’s approach – though they are! But to emphasise how poorly chosen and executed this work is. They’ve chosen a unrepresentative example and blundered in their workings, because they don’t understand how student loans, the graduate labour market and finance really work.

Had they chosen a more representative example, like a teacher starting in the region of £22-25,000 then they would still have the problem of massively underestimating likely repayments. A teacher who works for 30 years is more than likely to repay the equivalent of what was borrowed, but their nominal cash repayments would potentially be much higher than our friend who starts on £35,000. That results from making the majority of their repayments later, when each pound repaid has much less present value.

Here’s where we return to the problem I outlined earlier.

What should you do if the estimated cash total for repayments is higher than the outstanding balance?

The proposed statement offers no guidance, doesn’t even recognise the potential issues and as I’ve explained is likely to mislead borrowers by treating the present value problem of “today’s money” far too casually. So casually that they get the maths wrong!

A statement along the lines envisaged by MSE/RG certainly needs to present the projected salary pathway along with projected median earnings for some context. Here, I suggest looking at London Economics’ 2017 report for UCU.

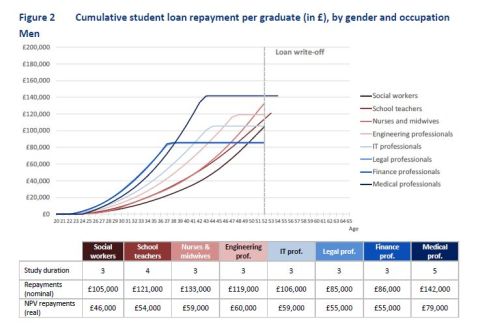

Although it predates the decision to raise the repayment threshold to £25,000, it illustrates well the size of cash repayments (“nominal”) before they are translated into net present values (NPV). It very helpfully shows salary pathways for various occupations as well as repayments cashflows.

The chart below is taken from that report. On this model, public sector workers are also earning over £100,000 by the time the write-offs occur and have made loan repayments in excess of £100,000 by the time the 30years is up!! (London Economics use official long-range projections for average earnings).

London Economics for UCU, The Impact of Student Loan Repayments on Graduate Taxes

London Economics for UCU, The Impact of Student Loan Repayments on Graduate Taxes

How Much?

How reassuring is it to have a brief statement that shows cash repayments of that order? In a detailed report, with a narrower audience, you can take care to explain the issue. But the space needed for a careful approach is not available in an annual statement for general readers.

There’s the real problem: the pay-off between detail and concision is not going to play out neatly. The explanation needed to walk a borrower through what they should legitimately conclude if the present value figure is higher than the outstanding balance defies inclusion in a three-page statement.

It is very difficult to see how the providing estimated repayments is helpful if former students do not understand some sophisticated finance. But then we’d have to open the question about what discount rate is appropriate for individuals …

A Step Back – first do no harm

Here though is where we should pause and realise that the complexity of loans should lead us to reach a different conclusion.

We have long recognised that student loans are confusing. We can now see that they are so confusing that a consumer affairs website and a sector lobby group can misunderstand them.

If you start from the principle, “first do no harm”, then you realise that there probably isn’t a presentational fix and we should instead reconsider the design of the scheme.

We should recognise that real interest rates are a design flaw that mislead borrowers into inappropriate comparisons. That is, the problem is bigger than can be addressed by presenting the statement differently.

We should now recognise that real interest rates encourage people into bad thinking and that bad thinking leads them into poor financial decisions (for example, remortgaging to pay children’s fees upfront).

Our student finance system should minimise its propensity to lead people into harmful financial decisions in the first place. Student loans should clearly be a good deal and no one should be left thinking that it might be better to accelerate repayments (and thereby inadvertently repay more!).

To my mind, such a principle trumps the additional repayments that real interest rates generate from higher earners. The real solution to the problem with which MSE and RG grapple is to reduce interest rates to CPI-only (or less).

No one should be confronted with a annual loan statement that misrepresents what a student loan commits you to. With CPI-only inflation, you can be sure that the value of your repayments will not exceed the value of your outstanding balance, even if you clear the balance in full before 30 years are up. Since an individual’s discount rate should be higher than CPI (at the very least since you need to factor in a value to reflect the death or disability insurance built-in to student loans), it won’t make sense for anyone to repay early. With a low interest rate, there would then be no reason to include spurious estimates about repayments in the statement.

No one should be weighing up whether paying upfront or making additional payments later makes sense for them.

We should cut interest rates to reduce the complexity of loans and reduce the likelihood of individuals losing money through bad decisions. The Treasury may not like it, but there is a broader public interest issue here.

Good stuff. It is obvious that, with high interest rates, **some** people will end up paying significantly more than the present value of what they have borrowed. But it is very difficult to judge whether it will apply to me and so I should pay off early, or ASAP, (or when…). I suspect that quite a lot of people will end up doing so, if never actually paying off the whole loan including interest. And won’t this risk deter some from borrowing to be a student at all? Surely barely-inflation interest rates have to be the sane, fair answer.