Some tips on writing about student loans

Student loans are complex and confusing. The design is now flawed as a result of a series of piecemeal decisions and the cost is too high for many and is too opaque.

But those pronouncing on loans need to avoid adding to the confusion and in particular need to avoid leaving listeners and readers with the impression that alternative options or early repayment are necessarily cheaper. For a small minority, they might be (but see below). But if you have money to spare, then look to pay rent, before tuition fees.

Some tips for writing about post-2012 student loans:

- Don’t talk about interest rates in isolation. They interact with repayment thresholds and write-off policies.

- Explain the interest rate taper. The top rate of 5.4% from September will only apply to those earning over £47,835pa (it’s not £41,000). Those earning below £26,576 face interest of 2.4%.

- Don’t compare student loans with commercial loans without giving full detail. Include reference to the built-in insurance for death and disability. In the case of a bad accident to a former student, student loans can be written off; a new mortgage that paid the tuition fees upfront won’t be.

- Always write: “Interest accrues”. Whether it will be repaid is a different matter and depends on lifetime earnings of the borrower.

- Explain the design behind the real rate of interest (even though it is flawed). The real rate of interest is there to keep higher earners repaying for longer. But only high earners will repay any of that interest. This is a design feature.

- Be clear on what a high earner is likely to earn – give an example. How many recent graduates earn over £26,576? What professions are they in?

- Emphasise that the “debt burden” from student loans is primarily repayments. Repeat that interest accruing is unlikely to be repaid.

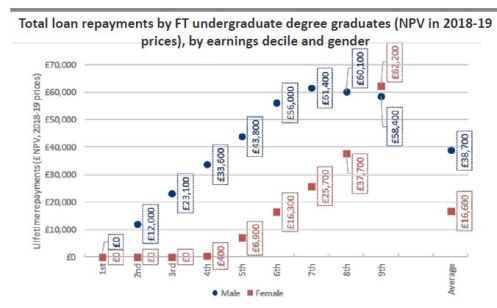

- Always set out the differences facing men and women. Use a chart like this one from London Economics.

Over 70% of women are projected to repay significantly less than they borrowed and almost 40% are expected to repay nothing. Paying upfront is a big gamble for women and making additional voluntary repayments make simply mean repaying more, if you are not likely to clear your balance.

Over 70% of women are projected to repay significantly less than they borrowed and almost 40% are expected to repay nothing. Paying upfront is a big gamble for women and making additional voluntary repayments make simply mean repaying more, if you are not likely to clear your balance. - Bear in mind that your listener or reader is very unlikely to have an idea of where they might sit in the deciles for estimated lifetime earnings. They are likely to overestimate their expected position.

- Use figures that adjust for the time value of money. Use government figures or figures from a respected outfit like London Economics or Institute for Fiscal Studies.

- Don’t use out of date figures or research. The repayment threshold was raised from £21,000 to £25,000pa two years ago and has increased annually since (it will be £26,575pa from April 2020). This reduces everyone’s mandatory repayments and gives more protection to low earners. It also made the scheme more expensive for government.

- Explain how it is that the government expects to lose money — almost 50p per £1 lent — even though the interest rates are what they are.

- If you must use the government figures for interest accruing, explain that this is a “fiscal illusion” (OBR). The government has been booking interest as income even though it may never be paid.

These figures will change shortly when the new ONS conventions come in. - Think carefully about what you’ve written. You don’t want to lead people into making bad financial decisions; for example, you don’t want to leave them with the impression that commercial borrowing is cheaper.

Trackbacks & Pingbacks