A story from the Bristol Post last week tells of plans for a new Bristol University campus.

With a first phase of development requiring £300m of investment, the campus will accommodate 5000 students and ‘house a new digital innovation hub and a business school’, with subsequent phases leading to a ‘a residential village’.

Such ambitious developments are not uncommon these days, but this announcement comes hot on the heels of Hefce’s annual warning about the sustainability of English university finances.

§16 The trend of falling liquidity (cash) and increasing sector borrowing reported previously is set to continue in the forecast period.

The sector expects its liquid funds to fall from £9.1 billion as at 31 July 2015 to £6.5 billion as at 31 July 2019, equivalent to 83 days of expenditure.

At the same time, the sector expects borrowing to increase from £8.3 billion at the end of July 2015 to £10.5 billion at the end of July 2019.

Borrowing levels are expected to exceed liquidity levels in all forecast years, with the sector expecting to be in a net debt position of £49 million at 31 July 2016, increasing to £3.9 billion at 31 July 2019. The trend of increasing borrowing and reducing liquidity is unsustainable in the long term.

Prior to 2012, the sector averaged a debt to income ratio of roughly 20% – a figure that had been stable for a decade. In the last five years this has climbed to 30%, a marked change given that universities, as charities, are expected to exercise prudence when it comes to capital investment and its associated risks.

Hefce include the following chart showing that ratio (projected for 2018/19) for each institution in the sector and how the sector average masks a large spread. (The one outlier excluded is likely to be Northampton, which has a debt:income ratio somewhere close to 300% after issuing a bond guaranteed by the Treasury and accessing loans from the Public Works Loan Board).

It is not clear if Bristol’s new plans were already factored into the submission on which Hefce based this chart. But its latest Financial Report (for 2015/16) shows that it already had £250m of long-term borrowing through two loan arrangements with Barclays. Against its annual income of £575m that leaves a debt:income ratio of 43%.

Bristol’s net current assets of £180m (at 31 July 2016) mean that it does not have significant levels of cash to contribute to the newly required £300m and it does not appear to have earmarked any assets for disposal (to raise funding for the new campus). The options would then appear to be third party financing (perhaps more likely for the second-phase of student accommodation) or further borrowing which would push it close to the 100% mark in the chart above.

In its annual report (p.10), Bristol notes: “HEFCE sets limits through its Memorandum of Assurance and Accountability process for borrowing by universities. Under this the University currently has a borrowing limit of £310m.”

This is a total borrowing limit based on a multiple of EBITDA (earnings before interest, tax, depreciation and amortization). There are two general points to note here. Hefce’s borrowing cap is due for review and it has indicated that it is likely to abandon EBITDA and move to a measure based on adjusted operating cashflow. But, more pertinently, Hefce is due to be wound up and replaced by the Office for Students.

The latter is being created by the Higher Education and Research Bill that has just completed its third reading in the House of Commons. Section 39 of the first draft of HERB gives OfS the power to set terms and conditions on grant or loan payments to registered HEI’s but no commitment to continue with the current MAA practice is stipulated. On a related note, Jo Johnson has just tabled an amendment giving the OfS power to monitor the financial sustainability of the sector. An explanatory note attached to the amendments reads:

This new clause, which is for insertion after clause 61, requires the OfS to monitor the financial sustainability of registered higher education providers who are in receipt of, or eligible for, certain kinds of public funding. It requires the OfS to include in its annual report a summary of conclusions which it draws from that monitoring regarding patterns, trends or other matters which it has identified relating to the financial sustainability of some or all of the providers monitored and which it considers are appropriate to be brought to the attention of the Secretary of State.

Given its preference for a market with provider ‘exit’, it would consistent for the government to prefer the current MAA arrangements to be relaxed and leave universities to make their judgements about external borrowing in peace.

There’s more to be said here, but I plan over the next year to use this blog to look in more detail at university debt and individual cases (a donation might sway me to look at a particular institution!).

One final point, Hefce notes that covenants on borrowing appear to be increasing which means that borrowers are setting conditions on universities that must be met if the lending is not to be revoked. These covenants relate to ‘financial performance’ and ‘balance sheet strength’. Its vital to note though that some bond covenants out there stipulated Hefce’s continued oversight of the sector through MAA’s as one of a pair of conditions that could trigger demands for bondholders’ funds to be returned. If the new monitoring arrangements are seen to breach that part of the covenant, then the second one becomes crucial: the university has to maintain an investment grade credit rating.

A blog by Warwick Mansell has alerted me to a speech given by Nick Timothy before the referendum, when he was head of the New Schools Network.

The relevance for HE lies in the manner in which he outlines his view of competition in education, particularly the idea that free schools should be opened in areas served by poor schools, rather than in areas suffering from a lack of places.

The following paragraph is critical for shedding further light on the topics of the two posts published on here this week about changes to HE policy after Theresa May’s elevation to prime minister.

The government is trying to create a market in the education system. This … is the right track for reform, but at the moment there’s a risk that we’re building in the potential for market failures too. A functioning market needs enough genuinely new entrants to challenge existing providers, enough capacity for competition to be meaningful, enough information for providers and users alike, ways of breaking up failing or monopolistic providers, and exit points for providers that aren’t doing a good enough job. The direction of travel is the right one, but there’s a lot that still needs to be done.

Picking over the bones of those sentences, I would focus on the emphatic use of ‘enough’ (remember proposed free schools go through an application process that has to evidence demand and need) and the more activist line on ‘breaking up’ failing or monopolistic providers. That is, market exit isn’t just about having plans in place if providers decide to shut down their education provision; there’s a role for the interventionist state in precipitating market exit if provision is deemed to be poor.

I’m afraid I’ve had to postpone this talk owing to ill health. (12 October)

The New Higher Education Settlement: Does it Add Up?

This summer’s White Paper for Higher Education, Success as a Knowledge Economy represents a new settlement for English universities and colleges. The White Paper heralds an intervention in settled notions of institutional autonomy and academic freedom as powers will be extended to establish a market for quality. The three-pronged justification for this reorientation is degree inflation, student dissatisfaction, and employer complaints about graduate abilities. Lurking in the background a further dimension has become clearer – the government as investor has not seen the expected return: an increase in graduate salaries. At the same time, the expansion of undergraduate places over the last two decades has not been accompanied by the predicted increase in British productivity, despite successive governments’ faith in the generic value of a degree…

View original post 112 more words

To follow the last post, I thought it might be worth making a few points based on Theresa May’s second speech to the Conservative Party conference.

May set out a vision of a meritocracy, a country ‘that works for everyone’, where if you ‘put in the hours and effort you will be rewarded’.

The emphasis was on fairness – a word repeated 15 times in the speech – and establishing a single, clear set of rules so that people could know how to get on in life.

May recognised – in a way that Osborne and Cameron had failed to do – that Britain is plagued by a sense that the ‘world works well for a privileged few’ but that the majority have seen their opportunities and standards of living decline in the last decade.

In this way, May tapped into common complaints about the apparent decline in social mobility. A crisis in the rules of the game of wealth accumulation (housing and pensions, primarily) that has underpinned the post-war social settlement.

This is sometimes described as a problem of intergenerational equity but I think it’s more accurate to see it as breakdown affecting the formation and reproduction of the middle classes. (I see this point as complementing Chris Dillow’s discussion of ‘May’s Challenge to Marxism’ – it is in the interests of capital to also seek ‘the defence and stability of the social order’).

More speculatively, what might May’s change of tack mean for higher education given the supposed centrality of higher education in improving life chances?

If May is consistent then I would expect to see a shift away from the idea that competition (with easier market exit and entry) will drive up quality and a move to shore up (or impose) standards so that ‘university means university’.

It’s not enough for there to be a single set of rules governing social mobility, those rules must be clear. That imperative runs counter to the consumer faced with an overwhelming choice of courses and institutions.

May announced a more interventionist policy with a bigger role for the state here, citing utility markets as a contender for reform.

That’s why where markets are dysfunctional, we should be prepared to intervene.

Where companies are exploiting the failures of the market in which they operate, where consumer choice is inhibited by deliberately complex pricing structures, we must set the market right.

Is there a more complex pricing structure than the HE fee-loan regime? What you borrow is not what you repay.

Moreover, from a certain perspective (that of the lender), the HE market looks dysfunctional with a large amount of misinvestment or even over-investment if you buy the analysis of groups like the Chartered Institute of Personnel and Development.

So I would now expect a more interventionist approach through the TEF and less inclination to let the market determine high quality courses.

If, as Amber Rudd announced, international students are going to be given clear signals about poor and high quality courses through the visa system, then I would expect something similar for Home students – probably through access to student loans.

Going back to Milton Friedman, the idea of a loan-funded system of higher education was always about the access to the professions (vouchers are appropriate to fund general boosts to citizenship and leadership).

The formation of human capital was meant to trump natural ability. I expect to see more questions and concerns about whether HE courses are imparting the skills and knowledge that warrants government loan support.

Following the Conservative party conference last week, the sector is reeling. It’s become clear that the government does not view higher education as an export success that should be supported in unqualified manner.

Amber Rudd, Home Secretary, announced a review of ‘the hundreds [sic] of different universities providing thousands of different courses across the country’ and whether the ‘generous offer’ of allowing universities to sponsor visas for international students ‘is really adding value to our economy’. This echoes comments I reposted on here last month – comments made in 2012 by Theresa May when she held Rudd’s post.

Rudd seems to see universities as good for attracting the ‘best talent’ to the UK, but is much less keen to see international fee-paying students as valued customers who can take their fees elsewhere. The final word of the next pair of sentences struck me:

I’m passionately committed to making sure our world-leading institutions can attract the brightest and the best. But a student immigration system that treats every student and university as equal only punishes those we should want to help.

It’s a strange choice of word, assuming somehow that non-UK students should be seen as opportunities for potential philanthropy (‘the deserving student’). She goes on:

So our consultation will ask what more can we do to support our best universities – and those that stick to the rules – to attract the best talent … while looking at tougher rules for students on lower quality courses.

Is the point here to flag up to international students that they would be better off avoiding ‘low quality’ courses. Is identifying courses as such to be part of the second phase of the Teaching Excellence Framework?

At the same time, the government also reiterated its wish to bring net migration down to below 100.000 per annum and that student numbers would be included in that target.

Many commentators have noted that Nick Timothy, May’s advisor, wrote last year about targeting university students to hit that migration measure. In an article for the Telegraph, Timothy appeared to identify 100 000 students at colleges and ‘non-Russell Group universities’ who would lose out under the ‘student visa cap’ he proposed. (That would leave 70 000 at Russell Group universities).

The Home Office estimates that the number of foreign students at Oxford and Cambridge is a little more than 4,000, while there are about 66,000 at the remaining Russell Group universities. That leaves more than 95,000 foreign students at non-Russell Group universities and more than 18,000 attending colleges.

That’s a startling proposal with the potential to damage finances. University of the Arts London for example gets one third of its annual income from non-EU fees.

This looks like unthinking vandalism but there is more to Timothy’s analysis. His Telegraph article cites two practices employed by universities that he thinks bend the rules.

Some have formed partnerships with colleges to allow foreign students to work as they study, circumventing the tough rules designed to stop economic migrants masquerading as college students. Other universities – which are often based hundreds of miles away from the capital – have set up London campuses to attract foreign “students”, many of whom simply want to work in the UK.

London campuses were one of the very few HE policy issues mentioned in the 2015 Conservative part manifesto. They were opposed to them – though we’ve yet to see any concrete policy measure brought to bear. (And will any spotlight be turned on Warwick’s Business School in the Shard or Liverpool’s London site?)

The first point, though, is the one that may offer most insight to what’s going on. Students at ‘Hefce designated’ universities (what we would have called ‘publicly funded’ a year or so back) have the right to work while studying, those at private colleges do not. Students at different institutions also face different post-study visa conditions on the right to stay and find or maintain employment.

What Timothy has to mind is a form of partnership agreement whereby a ‘Hefce designated’ institution sponsors the students at another college (perhaps as part of a franchising or validation arrangement) so that the students come in to the country as students of the established partner for the purposes of the visa, but are taught at the private partner.

It is a deal of this kind that was bound up in the travails at London Metropolitan four years ago. Theresa May intervened as Home Secretary after learning of LMU’s deal to sponsor 5000 London School of Business & Finance students each year. LMU had its licence to bring in international students suspended and the deal with LSBF was cancelled shortly after.

Do Timothy and May think such practices are widespread? I’m not sure. But it is clear that partnership arrangements of all kinds are much less common amongst the Russell Group than other universities.

And it’s clear that Theresa May’s focus on rules and fairness in her second conference speech may start to cast some shade on higher education institutions that are seen to be gaming the system or not up to scratch.

(The nominal minister for HE, Jo Johnson, seemed to be caught unawares by Rudd’s speech. Before June, it was necessary to watch the Treasury to understand HE policy, now it’s the Prime Minister’s Office setting the agenda).

I’m afraid I’ve had to postpone this talk owing to ill health. (12 October)

The New Higher Education Settlement: Does it Add Up?

This summer’s White Paper for Higher Education, Success as a Knowledge Economy represents a new settlement for English universities and colleges. The White Paper heralds an intervention in settled notions of institutional autonomy and academic freedom as powers will be extended to establish a market for quality. The three-pronged justification for this reorientation is degree inflation, student dissatisfaction, and employer complaints about graduate abilities. Lurking in the background a further dimension has become clearer – the government as investor has not seen the expected return: an increase in graduate salaries. At the same time, the expansion of undergraduate places over the last two decades has not been accompanied by the predicted increase in British productivity, despite successive governments’ faith in the generic value of a degree in human capital terms.

In this context, the government has commissioned research into the ‘value add’ of particular degrees and institutions which will dovetail with the development of new metrics and measures for the later phases of the teaching excellence framework, including tests for generic learning gain.

This talk will outline these developments and the contours of the next decade of HE policy as it is motivated by the government’s economic and financial considerations and what the resulting new ‘financialised’ framework will mean for the sector

Date: Thursday 20 October

Time: 1-2pm

Venue: Keele Hall – The Salvin Room Keele University

The talk is free and open to all.

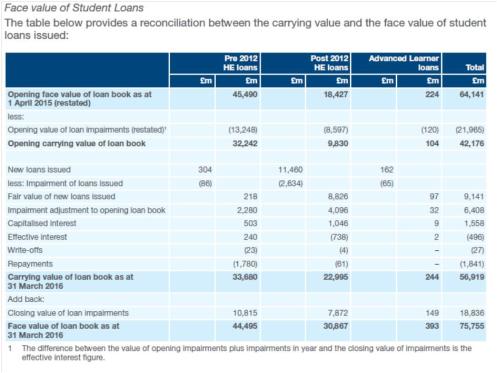

The 2015/16 BIS accounts state that a first sale of ‘pre-2012’ income contingent student loans is planned for 2016/17.

For the first time, the BIS accounts breakdown the loan book into ‘pre-2012’ and ‘post-2012’ loans, providing separate fair and face values for each category.

Click on image to enlarge

The fair value of loans earmarked for potential sale is therefore £34bn and BIS was aiming to raise around £12bn from a five-year sale programme.

It is important to note that the fair value – what the government thinks the loans are worth – is not what will be used in a value for money test. This is because the government uses a much higher discount rate to assess VfM: a sale could represent a substantial loss to government but still go ahead, since a higher discount rate means a lower valuation for future money.

Page 75 of the 2015/16 accounts:

Under accounting policies the amortised cost discount rate (currently 0.7 per cent) applies whereas the Department has agreed with HM Treasury that any decision to retain or sell an asset on the balance sheet the applicable discount rate is the social time discount rate (currently 3.5 per cent). The Department will also explore options to sell Green Investment Bank and the Government’s 33 per cent shareholding in Urenco.

The decision to change the reporting discount rate for student loans has sidestepped the dominant political debates about the sustainability of student finance with a classic accounting move, but this means that a central pillar of HE policy – selling the loans to clear the balance sheet and lower national debt – becomes less ‘presentable’.

Remember that the government only raised £3.3bn from the sale of Royal Mail shares and was thought to have missed out on millions. The government is entertaining an annual process that would generate more losses each year – but it’s hoping no one will pay too much attention.

For illustrative purposes here is a simple cash stream (£10 per year for 10 years) discounted at the two different rates (using RPI of 2.8%). You can see that an asset worth £83 would pass a VFM sale test if someone offered £72.

Click on image to enlarge

(ps this was updated as my original spreadsheet used the old plus 2.2 discount rate rather than the plus 3.5 VfM discount rate)

The 2015/16 annual accounts for now-defunct BIS were published back in July. They covered the financial year to 31 March 2016 (which can cause some confusion when comparing with other figures, such as SLC, that operate on the academic year).

Figures inside represent the first official updates to student loan estimates, valuations and projections since the Autumn, when the government confirmed it would freeze the loan repayment threshold for five years and lower the official financial reporting discount rate for loans to RPI plus 0.7% from ‘plus 2.2%’.

These measures were designed to secure the ‘sustainability’ of the student loan scheme and when combined they boosted the fair or carrying value of the student loan book by over £8bn.

At the end of March 2015, existing student loans had a face value of £64bn (what was nominally owed to government) and were expected to generate repayments equivalent to £42bn (‘fair’ or ‘carrying’ value) in net present value terms.

By the end of March 2016, the face value of the book had increased to £76bn with a fair value of £57bn, an increase for the latter of £15bn on the back of only £12bn issued in new loans. (FE Advanced Learner Loans account for £160m of the year’s new issuance).

The accounts report that the official RAB estimate for new loans issued is 23% (down from over 40%) and that the Treasury has set a target RAB of 28% (down from 35% to reflect the rebasing that the discount rate change has produced). 36% (a correction slip was issued in September 2016).

In a separate email, the BIS press office confirmed to me that the RAB allocations given to BIS in the 2015 Autumn Statement have been replaced by the following, which will pass over to DfE.

RDEL £bn

2016-17 2017-18 2018-19 2019-20

3.4 3.8 4.2 4.5

The Times reports today that Theresa May’s government is looking at ways ‘to examine how to reduce the number of international students coming to the UK’. This will require universities to develop funding models ‘not so dependent on international students’. (I teach once a week in one where 30% of its income comes from international fees).

It’s worth recalling the speech May made when she was Home Secretary to the 2012 Conservative Party conference. This took her spat with the BIS ministers public at the height the London Metropolitan University visa controversy.

They argue that more immigration means more economic growth. But what they mean is more immigration means a bigger population – there isn’t a shred of evidence that uncontrolled, mass immigration makes us better off.

… They argue, too, that we need evermore students because education is our greatest export product. I agree that we need to support our best colleges and universities and encourage the best students to come here – but to say importing more and more immigrants is our best export product is nothing but the counsel of despair.

We were elected on a promise to cut immigration, and that is what I am determined we will deliver.

Earlier this month, the Department for Education published a report on widening participation in England which compared entrants to HE by whether students were state-educated or privately educated.

The results in this report were widely reported as showing a recent fall in the number of state school students starting HE by 19 between 2010/11 and 2013/14. The Guardian’s coverage in particular linked this claimed fall to the introduction of higher tuition fees in 2012. (1) The claim has now been picked up by the two Labour leadership candidates.

This interpretation of the report is incorrect. Numbers entering HE by 19 remained stable at around 185,000 to 190,000 during a period when universities had recruitment capped.

So what does the report say?

70% of A level and equivalent students at state schools aged 17 in 2008/09 had entered HE by 19 in 2010/11. This dropped to 62% for the equivalent students by 2013/14.

The percentage change is due not to a fall in numbers entering HE (the numerator) but a large change in the denominator: the numbers of 17 year-olds in post-16 education increased significantly between 2008/09 and 2011/12.

Here are the relevant tables (the ‘Total state’ row is the relevent one):

2010/11

Number progressing to HE from all state schools = 186,065

Total aged 17 studying for A levels or equivalent = 264,230

Percentage = 70%

2013/14

Number progressing to HE from all state schools = 187,075

Total aged 17 studying for A levels or equivalent = 300,905

Percentage = 62%

As you can see, the numbers of state school educated students going into HE by 19 has increased very slightly. You might reasonably argue that this percentage is too low (85% of privately educated students continue to go on to HE), but this is very different from claiming a fall in state-educated HE entrants that can be attributed to tuition fees.

The real test on this particular measure of widening participation is what results from uncapping recruitment and the expansion of providers.

(1) I wrote to the Guardian last Monday requesting a correction but no response has been forthcoming.