On Tuesday, the department for Business, Innovation & Skills published its annual accounts for 2014/15 along with a revised ‘simplified’ student loan repayment model, which enables those interested to play around with student loan policy and look at the impacts.

The headline from the accounts is that the resource accounting and budgeting charge for post-2012 loans remains ‘around 45 per cent’, where it has been since March 2014. (The RAB charge presents the resource needed to cover the fact that loans are estimated to be worth less than the money used to create them. The loans are ‘impaired’ in the jargon.).

Detail in the accounts shows that new loans issued between April 2014 and March 2015 came to £10.655billion and that the ‘impairment’ required was £4.619billion. The latter is 43% of the value of loans issued, but this figure is brought down because last year’s loan issue contains loans made to those still paying £3000 pa in tuition fees.

Overall, the government now holds HE loans with a face value of £64billion (the total amount of outstanding loan balances ) but an estimated ‘carrying value’ or ‘fair value’ of £42billion (the net present value of repayments generated by those balances).

That is higher than expected for one reason. The value of existing loans has been revised upwards by £2.756billion since 2013/14

There are two contributing factors:

- Changed forecasts for RPI, bank base rates and earnings improved the value of ‘pre-2012 loans’ by £1.36bn. For example, lower than expected RPI meant that the repayment threshold for pre-2012 loans will be lower than previously anticipated: £17 333 in 2015/16. (Lower RPI also means a lower discount rate).

- BIS has developed a new iteration of its repayments model. STEP3 (Stochastic Earnings Path) has improved projected repayments on existing loans by £1.4bn. A guide to these changes can be found with the new simplified model. Changes involve making a series of ‘more realistic’ assumptions about lifetime earnings ‘pathways’ and the likelihood of unemployment. But the new model also ‘ uses course subject and institution information [of recent graduates] to improve the forecasting of earnings in early repayment years’. A precursor to the Teaching Excellence Framework?

The picture on student loans has therefore improved compared to last year but underscores the volatility surrounding attempts to predict future loan repayments. In 2013/14 the value of existing loans plummeted by £2bn as a result of revisions to modelling (STEP 2). The latest iteration has recovered 70% of that loss, while changes in macroeconomic forecasts have improved the overall picture by £750million.

The previous post and this one show that we are still in the very early days of the new funding regime and in some senses it won’t hit operational maturity for another decade or two. Another revision to STEP is not planned (STEP replaced HERO in 2013).

The Office for Budgetary Responsibility has corrected the tables it provided on student loans in last week’s Economic & Fiscal Outlook, which was published to accompany the Budget. A full explanation can be found here.

This table separates ‘English’ loans from the rest of the UK as well as the proposed English postgraduate loans. The row marked ‘maintenance loans’ only scores those loans created to cover the cuts to maintenance grants in England. All years are financial years (April-March) rather than academic years.

English repayments decline after 2017/18 owing to the impact of selling a proportion of the student loans issued before 2012 to the private sector. This remains the ‘expected’ policy of this government – with the first tranche of sales expected at the end of 2015/16.

The expected proceeds from any sale (c. £11.5bn) are dwarfed by the annual ‘net cash outlay’ requirements (first row) over the course of Parliament. This represents the difference between annual ‘gross cash outlay on new loans’ – which rises to £20.6biillion by 2020/21 – and ‘gross cash repayments received’.

This net cash outlay adds to the public debt over and above whatever contribution the ‘deficit’ makes. Understanding the Treasury position on loans depends on seeing these projected cashflows and their effect on the ‘pathway’ of public sector net debt, rather than whatever ‘loss’ on loans the ‘RAB charge’ represents.

For more detail see my Accounting and Budgeting of Student Loans.

Despite the enormity of yesterday’s budget announcement, it transpires that BIS still has to locate £450m of cuts in this financial year (2015-16).

The abolition of maintenance grants for new starters in 2016/17 will ultimately take from annual expenditure an amount close to £1.6bn per year. This reduces the current measure of the deficit by the same amount despite the replacement of grants by an equivalent amount of maintenance loans. This leads to the cumulative saving announced in the Budget document – £2.5bn by 2020/21.

Osborne cited a figure of £3bn per year, but this relates estimates of the cost of a new commitment outlined by Jo Johnson earlier this month: Cameron has stipulated that new freedoms for universities to recruit must see ‘double the proportion of disadvantaged young people entering higher education by 2020 from 2009 levels’.

That is, maintenance grants are currently means-tested so having more students from less wealth-off families would see an increase in maintenance grant. This was taken to be ‘unsustainable’. The OBR models annual loan issuance to increase by £3bn to compensate.

Loan issuance for the whole of the UK looks set to clear £20bn per annum by 2020, while repaymenys languish somewhere around £2.5bn. Despite the ‘deficit saving’, these large shortfalls will add significant upwards pressure to the public debt until repayments improve. Freezing the repayment threshold for all those with loans who started after 2011 would improve repayments more quickly. It’s these cashflows and the impact they have on public debt which concern the Treasury rather than the specific ‘RAB’ attached to each year’s issue of new loans. BIS was already under pressure to improve loan ‘performance’ and it’s not yet clear how to assess the impact on its future budgets. We’ll only have enough information when the Autumn spending review comes around. The Treasury is very happy to switch grant expenditure to loans, but it is still very concerned about the impact of loans on the future ‘UK debt pathway’ (see the eary sections of yesterday’s Budget on ‘the long-term debt challenge’).

But back to the £450m cuts. A BIS spokesperson told Times Higher Education

“We are continuing to work on how to implement the £450 million savings, across BIS budgets, announced by the chancellor on 4 June; on higher education we will ask Hefce [the Higher Education Funding Council for England] to implement funding reductions in a way that does not undermine the viability of institutions.”

It is hard to see the remaining teaching grant for STEM subjects being affected, but Student Opportunity Funds may go with Hefce/BIS seeking to have universities cover more of those costs from fee income.

This blog is run on a voluntary basis with no commercial or outside support.

Things are hotting up in English HE and I will aim to provide an alternative take. Please do consider donating.

Please see About page for more details.

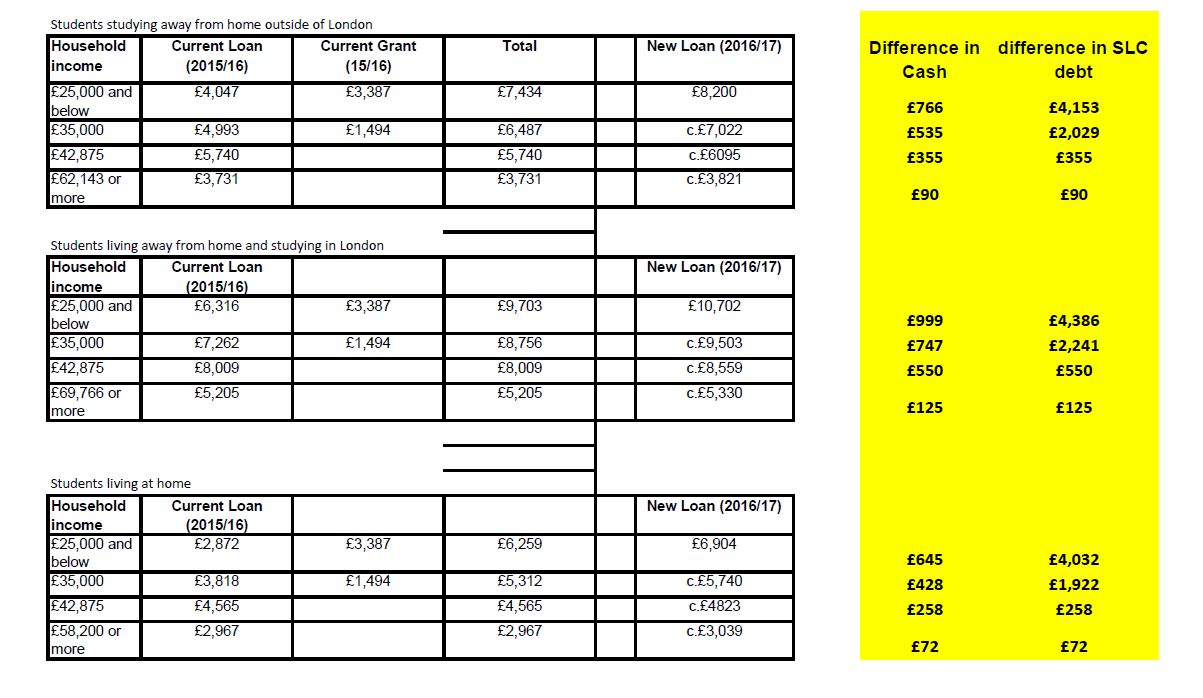

I have received the maintenance loans breakdown from the Treasury. I have added a few columns to illustrate the difference in annual cash received and the difference in associated debt (before interest is applied). This policy affects new starters in 2016/17, students already studying stay on the mix on grants and loans.

It looks like students from the poorest backgrounds will graduate with the highest debts. I’m looking forward to comment from those who’ve been berating the SNP’s track record in Scotland. It doesn’t look as stark as this.

click on the image below to see full version

Update

I have been asked to explain the reference to the Scottish National Party. In order to maintain free tuition for undergraduate study, the SNP rejigged its maintenance support provision for students. This has led many commentators to criticise Scotland for having ‘the lowest rate of grant in Western Europe’ and being the only place in the UK where those from the poorest backgrounds have the highest graduating debts.

The implication was always that this was the cost of being tuition free – putting a greater burden on the poor. Yesterday’s announcements makes clear that England will have no grant, the poorest will have the highest graduating debts and we will have the highest tuition fees.

The full text of the budget announces:

To ensure that the long term costs of the student loan book remain affordable and transparent, the government will consult on freezing the loan repayment threshold for five years and review the discount rate applied to student loans and other transactions to bring it into line with the government’s long-term cost of borrowing.

The intention to freeze the loan repayment threshold at £21 000 may apply to all those who have started undergraduate study since 2012 and taken out loans. That’s been the recommendation of a number of recent pamphlets. I’m not alone in thinking this retrospective price hike threatens goodwill towards HE. But university managements are in favour because it is likely to protect their income at the expense of graduates.

The discount rate announcement has also been flagged up in various places and is discussed by me in detail in a recent pamphlet for Higher Education Policy Institute.

In brief, Osborne’s switch from maintenance grants to loans will send estimates of loan non-repayment spiralling (little of the new loans issued will be repaid without tightening of repayment conditions). This will look bad. Lowering the discount rate would improve the headline numbers.

But that’s not the end of the story. The discount rate affecting student loans has been under review for a while and we were expecting a new one in Autumn, when the spending review sets departmental budgets for the parliament. If the rate is changed in such a way as to lower the headline rate, BIS’s budget would be adjusted downwards accordingly. We cannot assess the impact of these announcements on the department’s finances until we see the detail in the Autumn.

A second point is that there was still no confirmation of a loan sale today – it remains ‘expected’ but not confirmed. Any significant chance to the discount rate would make the loss on any sale look much worse as the discount rate under discussion here affects the value of the loans as they are recorded in the accounts.

Osborne’s speech today seemed to indicate the abolition of means-testing for student loans promising ‘all students from all backgrounds’ access to an annual loan of £8200.

The text of the Budget suggests otherwise adding the caveat:

2.202 Student maintenance – Maintenance loan support will rise for students from low and middle income backgrounds up to £8,200 a year studying away from home, outside London. From the 2016-17 academic year, maintenance grants will be replaced with maintenance loans for new students from England, paid back only when their earnings exceed £21,000 a year.

I am waiting on some figures from the Treasury to assess what this means exactly. But a quick calculation suggests that a student studying away from home outside London from 2015 whose family income is under £25 000 would currently receive £3 387 in grant and a maximum of £4 047 in loan. So this policy might see students having an extra £766 per year while studying but much larger graduating SLC debts.

There were 3 big announcements for English HE in today’s budget.

- the maximum tuition fee for undergraduate study would rise in line with inflation for institutions that can demonstrate high quality teaching. This is likely to reference the newly announced ‘Teaching Excellence Framework’ which will recognise ‘excellence and innovation’ in teaching.

- Government will consult on freezing the repayment threshold for all those who have taken out student loans since starting undergraduate study 2012. The £21 000 threshold was meant to rise in line with earnings after 2016. This represents a retrospective price hike but is needed to keep control of the loan repayments as a result of the third announcement.

- Maintenance grants will be abolished and replaced by a maximum maintenance loan of £8 200 for those starting undergraduate study in 2016/17. This appears to involve the abolition of means teaching as ‘to ensure university is affordable to all students from all backgrounds, we’ll increase the maintenance loan available to £8,200 – the highest amount of support ever provided’.Current levels are:

-

Full-time student Loan for courses from September 2014 Loan for courses from September 2015 Living at home Up to £4,418 Up to £4,565 Living away from home, outside London Up to £5,555 Up to £5,740 Living away from home, in London Up to £7,751 Up to £8,009

I have updated my Teaching page to reflect the various courses I’ll be involved with this summer and in 2015/16.

We’re developing some innovative mathematics courses that require no prerequisites and range from drawing-led investigations of geometry to philosophy of mathematics and Borges’s literary interests. They are open to the public and offered at CityLit or Central Saint Martins.

I have penned a short opinion piece in response to yesterday’s THE Willetts-fest. That should appear in next week’s issue and is mainly concerned with something i’ve been warning about for a while – the future-policy contingency of students loans. At last, Willetts has admitted that changing terms for existing borrowers may be crucial to the sustainability of the curent iteration of the fee-loan regime.

I agree with Martin Lewis on fundamental opposition to varying terms for existing borrowers. You might also want to note Greg Clark’s response to my question on this point in April: ‘The strength of our system is that it is robustly sustainable – as the OECD has confirmed – without any changes in terms being needed.’

Here, I’ll just quickly deal with a technical point about discount rates (quick explainer here). The government chooses to discount expected future loan repayments by RPI plus 2.2%. Over the last few years, several commentators have argued that the Treasury is ‘overcharging’ BIS because the government’s cost of borrowing is much lower. Willetts takes up there cause in his concluding paragraphs:

Finally, the government should shift to a more sensible discount rate for RAB charge calculations linked to the actual cost of borrowing as shown in index-linked gilts.

… The Institute for Fiscal Studies estimates that the freezing of the repayment threshold together with correcting the discount rate would reduce the RAB charge to about 15 per cent. Together with the structure of future quinquennial reviews, these measures would put an end to a sterile and confused debate about the RAB charge by showing that England’s model of higher education funding is flexible and sustainable.

I will make three quick points. For those interested, I discuss discount rates in more detail in my recent pamphlet for HEPI.

People tend to simply read the RAB charge as an estimate of ‘losses’ to government. If it were, then the IFS/Willetts point would be correct. But the RAB is really about budgeting and the discount rate is a long-term budgeting parameter rather than something specific to student loan estimates. Crucially, if the discount rate were lowered, then BIS would accordingly receive less resource to cover RAB. That is, the headline figures might be lower, but BIS would, all else being equal, still face a budget shortfall and the problem of improving loan repayments.

The second is probably more important, but also more technical. We may well see a new long-term discount rate in the Autumn spending review, but maybe not one tied to index-linked gilts. In recent months, the Treasury has put forward several proposals to switch its discounting away from a proxy for ‘cost of borrowing’ to measures that track projected GDP growth. Those interested can browse the various papers put before the Financial Reporting Advisory Board. I have struggled to find authoritative commentary on this matter – largely because it’s even more arcane than RAB. But for loans if GDP growth is projected to return to trend and something like that is used for student loans, then we may see little difference in the discount rate figure. (I would welcome comment from anyone who knows about government discounting).

Finally, were the relevant discount rate to be revised down then it would present difficulties for government seeking to present a student loan sale as value for money. Although the ‘value for money’ test uses a separate rate based on ‘social time preference’, losses would be valued according to financial reporting and budgeting rate. A lower discount rate now would make a sale programme look pretty bad. (Again, I have treated this in more detail in a recent article for London Review of Books).